UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31 , 2025

OR

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE TRANSITION PERIOD FROM TO

Commission File Number 001-42437

(Exact name of Registrant as specified in its Charter)

| | | |

| (State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

| | | |

| (Address of principal executive offices) | | (Zip Code) |

Registrant’s telephone number, including area code: +61 7 3152 3200

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

| | | The |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

YES ☐ ☒

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act.

YES ☐ ☒

Indicate by check mark whether the Registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

☒ NO ☐

Indicate by check mark whether the Registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit such files).

☒ NO ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| | ☒ | Smaller reporting company | |

| Emerging growth company | | | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

YES ☐ NO ☒

The registrant was no t a public company as of the last business day of its most recently completed second fiscal quarter and, therefore, cannot calculate the aggregate market value of its voting equity held by non-affiliates as of such date.

The number of shares of Registrant’s Common Stock outstanding as of February 25, 2026 was 97,232,054 .

| TABLE OF CONTENTS | |||

| Page | |||

| 6 | |||

|

Item 1.

|

6 | ||

|

Item 1A.

|

27 | ||

|

Item 1B.

|

56 | ||

|

Item 1C.

|

56 | ||

|

Item 2.

|

57 | ||

|

Item 3.

|

57 | ||

|

Item 4.

|

57 | ||

| 58 | |||

|

Item 5.

|

58 | ||

|

Item 6.

|

58 | ||

|

Item 7.

|

59 | ||

|

Item 7A.

|

66 | ||

|

Item 8.

|

67 | ||

|

Item 9.

|

107 | ||

|

Item 9A.

|

107 | ||

|

Item 9B.

|

108 | ||

|

Item 9C.

|

108 | ||

| 108 | |||

|

Item 10.

|

108 | ||

|

Item 11.

|

115 | ||

|

Item 12.

|

123 | ||

|

Item 13.

|

129 | ||

|

Item 14.

|

132 | ||

| 132 | |||

|

Item 15.

|

132 | ||

|

Item 16.

|

134 | ||

INTRODUCTION

Prior to the consummation of our initial public offering in December 2024, we completed a series of reorganization transactions (the “Reorganization”). Unless otherwise indicated or context otherwise requires in this Annual Report on Form 10-K (this “Form 10-K”), all references in this Form 10-K to the “Company,” “Anteris,” “Anteris®,” “we,” “us” and “our” refer to Anteris Technologies Pty Ltd (“ATPL”, formerly Anteris Technologies Ltd) prior to the Reorganization and Anteris Technologies Global Corp. (“ATGC”) after the Reorganization, and for purposes of this Form 10-K:

•

“ADAPT® anti-calcification tissue” refers to the tissue produced by the ADAPT® tissue engineering process, which transforms xenograft tissue (bovine heart tissue) into a durable bioscaffold which Anteris uses in its DurAVR® THV to mimic human tissue in aortic valve replacement.

•

“Aldehydes” refers to organic compounds.

•

“Aortic stenosis” refers to the narrowing of the aortic valve restricting the flow of blood from the left ventricle (lower chamber of the heart) to the aorta (main artery).

•

“Bioscaffold” refers to a durable structure engineered from biological material.

•

“Coaptation” refers to the portion of the leaflets that touch when the aortic valve is in the closed position.

•

“ComASUR® Delivery System” refers to the balloon expandable system which provides controlled deployment and accurate placement of the DurAVR® THV, designed to achieve precise alignment with the heart’s native commissures to achieve ideal valve positioning.

•

“Commissure alignment” refers to the position of the transcatheter aortic valve replacement leaflets in line with the anatomical orientation of the recipient’s native valve leaflets.

•

“Commissures” refers to where the valve leaflets are attached to the aortic wall inside the aortic sinus of Valsalva.

•

“Cytotoxicity” refers to toxicity to cells.

•

“Doppler velocity index” and “DVI” refer to the index that expresses the EOA as a proportion of valve area, with DVI representing the physical ratio of a patient’s aortic valve area to the left ventricular outflow tract area. A higher DVI indicates improved blood flow through the aortic valve. DVI is independent of the flow state (like gradient) and diameter (like EOA).

•

“DurAVR® THV” refers to a transcatheter heart valve (“THV”) developed by Anteris. It is a novel, biomimetic (meaning human-like) valve made from a single-piece of native-shaped ADAPT® tissue and is used for the treatment of aortic stenosis. The DurAVR® THV (new aortic valve) is placed within the diseased aortic valve via a minimally invasive procedure.

•

“Effective orifice area” and “EOA” refer to the smallest cross-sectional area of the aortic valve opening that is available for blood flow. A larger EOA reduces the work the left ventricle (heart chamber) must do to pump blood through the valve. Patients with severe aortic stenosis typically have an EOA of ≤ 1 cm2.

•

“Exercise capacity” refers to a measure of a patient’s exercise ability, measured in clinical trials by a six minute walk test (“6MWT”), which scores a person on the distance they can cover in six minutes of walking.

•

“Flow displacement” and “FD” refer to a marker of flow eccentricity in the ascending aortic root. Flow in the ascending aortic root is mainly laminar with a flow displacement ranging from 6 – 15% only. A higher degree of FD reflects abnormal turbulent flow.

•

“Flow reversal ratio” or “FRR” is calculated at peak systole in the ascending aorta. At this point there should be almost no backward flow, and any backward flow is considered abnormal. FRR represents the ratio of backward and forward flow at peak systole.

•

“Hemodynamics” refers to how blood flows through the blood vessels.

•

“Laminar flow” refers to a smooth, streamlined flow of blood. In a healthy heart, aortic flow is predominantly laminar during systole (when the left ventricle contracts and pumps blood into the aorta). Abnormal aortic flow is associated with turbulence, which can increase the risk of morbidity and increase the stress on the valve leaflets leading to increased wear and tear and subsequent structural valve deterioration.

•

“Mean pressure gradient” and “MPG” refer to the average pressure across the aortic valve between the left ventricle and aorta. Patients with severe aortic stenosis have MPG ≥ 40 mmHg. Post-TAVR MPG is expected to decrease, which indicates that the left ventricle is not working as hard to pump blood through the aortic valve.

•

“Transcatheter aortic valve replacement” or “TAVR” refer to a minimally invasive procedure for the treatment of aortic stenosis. A new aortic valve is placed inside the diseased valve, meaning the old, damaged valve is not removed.

•

“ViV” refers to valve-in-valve.

•

“Xenograft” refers to a tissue that is derived from a species that is different from the recipient of the specimen, meaning tissue from animal species.

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

All statements in this Form 10-K, other than statements of historical facts, including statements regarding our future results of operations and financial position, business strategy, product development, and plans and objectives of management for future operations, are forward-looking statements. These forward-looking statements generally are identified by the words “believe,” “project,” “expect,” “anticipate,” “estimate,” “intend,” “budget,” “target,” “aim,” “strategy,” “plan,” “guidance,” “outlook,” “may,” “should,” “could,” “will,” “would,” “will be,” “will continue,” “will likely result” and similar expressions, although not all forward-looking statements contain these identifying words. Forward-looking statements, which are subject to risks, include, but are not limited to, statements about:

•

our current and future research and development (“R&D”) activities, including clinical testing and manufacturing and related costs and timing;

•

our product development and business strategy, including the potential size of the markets for our products and future development and/or expansion of our products in our markets;

•

our ability to commercialize products and generate product revenues;

•

any statements concerning anticipated regulatory activities, including our ability to obtain regulatory clearances;

•

our R&D expenses;

•

risks facing our operations and intellectual property;

•

sufficiency of our capital resources; and

•

our ability to raise additional funding when needed.

We have based the forward-looking statements contained in this Form 10-K largely on our current expectations, estimates, forecasts and projections about future events and financial trends that we believe may affect our financial condition, results of operations, business strategy and financial needs. In light of the significant uncertainties in these forward-looking statements, you should not rely upon forward-looking statements as predictions of future events. Although we believe that we have a reasonable basis for each forward-looking statement contained in this Form 10-K, we cannot guarantee that the future results, levels of activity, performance or events and circumstances reflected in the forward-looking statements will be achieved or occur at all. You should refer to the section titled “Risk Factors” for a discussion of important factors that may cause our actual results to differ materially from those expressed or implied by our forward-looking statements. Furthermore, if our forward-looking statements prove to be inaccurate, the inaccuracy may be material.

The forward-looking statements made in this Form 10-K relate only to events as of the date on which the statements are made. Except as required by law, we undertake no obligation to publicly update any forward-looking statements, whether as a result of new information, future events or otherwise. The Private Securities Litigation Reform Act of 1995 and Section 27A of the Securities Act of 1933 (the “Securities Act”), do not protect any forward-looking statements that we make within this Form 10-K.

You should read this Form 10-K and the documents that we reference in this Form 10-K completely and with the understanding that our actual future results may be materially different from what we expect. We qualify all of the forward-looking statements in this Form 10-K by these cautionary statements.

This Form 10-K contains certain data and information that we obtained from various publications, including industry data and information from Future Market Insights, Inc. (“FMI”). Statistical data in these publications also include projections based on a number of assumptions. The global, North American and European TAVR markets may not grow at the rate projected by market data or at all. Failure of the global, North American and European TAVR markets to grow at the projected rate may have a material and adverse effect on our business and the market price of our Common Stock, par value $0.0001 per share (“Common Stock”), and CHESS Depository Interests (“CDIs”). All references in this Form 10-K to Common Stock shall include the shares represented by CDIs unless the context suggests otherwise. In addition, the nature of the medical technology industry results in significant uncertainties for any projections or estimates relating to the growth prospects or future condition of our industry. Furthermore, if any one or more of the assumptions underlying the market data are later found to be incorrect, actual results may differ from the projections based on these assumptions. You should not place undue reliance on these forward-looking statements.

CAUTIONARY NOTE REGARDING INDUSTRY AND MARKET DATA

This Form 10-K includes information concerning the Company’s industry and the markets in which it operates that is based on information from various sources including public filings, internal company sources, various third-party sources and management estimates. In addition, this Form 10-K contains information from a report prepared by FMI, a market research firm that we commissioned to provide information on the global transcatheter heart valve replacement market. Management estimates regarding the Company’s position, share and industry size are derived from publicly available information and its internal research and are based on a number of key assumptions made upon reviewing such data and the Company’s knowledge of such industry and markets, which it believes to be reasonable. In some cases, we do not expressly refer to the sources from which this information is derived. While the Company believes the industry, market and competitive position data included in this Form 10-K is reliable and is based on reasonable assumptions, such data is necessarily subject to a high degree of uncertainty and risk and is subject to change due to a variety of factors, including those described in sections titled “Special Note Regarding Forward-Looking Statements,” “Risk Factors” and elsewhere in this Form 10-K. These and other factors could cause results to differ materially from those expressed in the estimates included in this Form 10-K. The Company has not independently verified any data obtained from third-party sources and cannot assure you of the accuracy or completeness of such data.

RISK FACTOR SUMMARY

Investing in shares of our Common Stock involves a high degree of risk. You should carefully consider the following risks and uncertainties, together with all of the other information contained in this Form 10-K, including the section titled “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our audited consolidated financial statements and related notes included elsewhere in this Form 10-K, together with our other publicly available filings with the Securities and Exchange Commission (the “SEC”). The occurrence of any of the following risks, or of additional risks and uncertainties not presently known to us or that we currently believe not to be material, could materially and adversely affect our business, financial condition, reputation, and results of operations. Set forth below is a summary of some, but not all, of the principal risks we face:

•

We have a history of operating losses and may not achieve or maintain profitability in the future.

•

Unsuccessful clinical trials or procedures relating to our products could have a material adverse effect on our prospects.

•

If we are unable to successfully identify, develop, obtain and maintain regulatory clearance or approval for and ultimately commercialize any of our current or future products, or experience significant delays in doing so, our business, financial condition and results of operations will be materially adversely affected.

•

Even if a product receives regulatory clearance or approval, it may still face development and regulatory difficulties that could delay or impair future sales of products.

•

Even with regulatory clearance or approval to bring a product to market, our profitability may be impacted by ongoing coverage and reimbursement determinations by government health care programs and other third-party payors for our products, or procedures and services that rely on our products.

•

Our products are in development and may not achieve market acceptance, if approved, which could limit our growth and adversely affect our business, financial condition, and results of operations.

•

We may find it difficult to enroll patients in our clinical trials, and patients could discontinue their participation in clinical trials, which could delay or prevent clinical trials and make those trials more expensive to undertake.

•

We operate in a highly competitive and rapidly changing industry, and if we do not compete effectively, our business will be harmed.

•

The success of many of our products may depend upon the knowledge and experience of certain key physicians and heart valve centers.

•

We rely on third parties to conduct our clinical trials and preclinical studies. If these third parties do not successfully carry out their contractual duties, comply with applicable regulatory requirements or meet expected deadlines, our development programs and our ability to seek or obtain regulatory clearance and approval for or commercialize our products may be delayed.

•

We are subject to various risks relating to international activities that could affect our profitability, including risks associated with currency fluctuations and changes in foreign currency exchange rates.

•

Any failure to protect our information technology infrastructure and our products against cyber-based attacks, network security breaches, service interruptions, artificial intelligence or data corruption could materially disrupt our operations and adversely affect our business and operating results.

•

Artificial intelligence technologies could present business, compliance and reputational risks.

•

Increased emphasis on environmental, social, and governance matters may have an adverse effect on our business, financial condition, results of operations and reputation.

•

We could become exposed to product liability claims that could harm our business, and we may be unable to obtain insurance coverage at acceptable costs and adequate levels.

•

Use of our products in unapproved circumstances could expose us to liabilities.

•

Our products and operations are subject to extensive government regulation, including environmental, health and safety regulations, which could result in substantial costs. Furthermore, any failure to comply with applicable requirements could harm our business.

•

Healthcare policy changes may have a material adverse effect on us.

•

We could be exposed to significant liability claims if we are unable to obtain insurance at acceptable costs and adequate levels or otherwise protect ourselves against potential product liability claims.

•

Tax laws, regulations, and enforcement practices are evolving and may have a material adverse effect on our results of operations, cash flows and financial position.

•

Our success depends on our ability to protect our intellectual property and our proprietary technology.

•

Intellectual property rights of third parties could adversely affect our ability to commercialize our products.

•

Our reliance on third parties requires us to share our trade secrets, which increases the possibility that a competitor will discover them or that our trade secrets will be misappropriated or disclosed.

•

Obtaining and maintaining our patent protection depends on compliance with various procedural, document submission, fee payment and other requirements imposed by governmental patent agencies, and our patent protection could be reduced or eliminated for non-compliance with these requirements.

•

Any difficulty with protecting our intellectual property could diminish the value of our intellectual property rights in the relevant jurisdiction.

•

Medtronic plc (“Medtronic”) beneficially owns a significant equity interest in us and its interests may conflict with our or your interests.

•

We will require substantial additional future financing and, until commercialization of our products, our cash burn in future periods may be higher than anticipated. We may be unable to raise sufficient capital in future financings, including to account for unanticipated cash burn, which could have a material impact on our R&D programs or commercialization of our products.

•

Our Common Stock is listed on The Nasdaq Global Market (“Nasdaq”), but the market price and trading volume may continue to fluctuate and remain limited in terms of liquidity.

•

Our Second Amended and Restated Certificate of Incorporation (“Charter”) and Amended and Restated Bylaws (“Bylaws”) contain anti-takeover provisions that could delay or discourage takeover attempts that stockholders may consider favorable.

Overview

Anteris is a structural heart company dedicated to revolutionizing cardiac care by pioneering science-driven and measurable advancements to restore heart valve patients to healthy function. Our lead product, the DurAVR® THV System, was designed in collaboration with the world’s leading interventional cardiologists and cardiac surgeons to treat aortic stenosis — a potentially life-threatening condition resulting from a narrowing of the aortic valve. The balloon-expandable DurAVR® THV is the first biomimetic valve, which is shaped to mimic the performance of a healthy human aortic valve and aims to replicate normal aortic blood flow. Our DurAVR® THV System consists of a single-piece, biomimetic valve made with our proprietary ADAPT® tissue-enhancing technology and deployed with our balloon expandable ComASUR® Delivery System. ADAPT® is our proprietary anti-calcification tissue shaping technology that is designed to reengineer xenograft tissue into a pure, single-piece collagen bioscaffold. Our patented ADAPT® tissue has been clinically demonstrated to be calcium free for up to 10 years post-procedure, according to Performance of the ADAPT-Treated CardioCel® Scaffold in Pediatric Patients With Congenital Cardiac Anomalies: Medium to Long-Term Outcomes, published by William Neethling et. al., and has been distributed for use in over 55,000 patients globally in other indications. Our balloon expandable ComASUR® Delivery System, which was developed in consultation with physicians, is designed to provide precise alignment with the heart’s native commissures to achieve accurate placement of the DurAVR® THV. As of December 2025, more than 130 patients have been implanted with the DurAVR® THV worldwide.

Aortic stenosis is one of the most common and serious valvular heart diseases. It is fatal in approximately 50% of patients if left untreated after two years, and no pharmacotherapy is available to treat this disease. Aortic stenosis causes a narrowing of the heart’s aortic valve, which reduces or blocks the amount of blood flowing from the heart to the body’s largest artery, the aorta, and from there to the rest of the body. Minimally-invasive transcatheter aortic valve replacement (“TAVR”), which the U.S. Food and Drug Administration (“FDA”) initially approved in 2011 for high surgical risk patients, has emerged as an alternative to open-heart surgery. In 2019, the FDA also approved TAVR for use in low-risk surgical patients. These low-risk surgical patients are often younger persons within the geriatric population that require heart valves with longer durability and pre-disease hemodynamics for an improved quality of life. More generally, patients with aortic valve stenosis are now being diagnosed at a younger age. Yet, according to a publication in The Journal of American Medical Association, only 15-20% of severe aortic stenosis cases are treated today.

While previous generations of TAVRs were designed for older, high risk patients, our DurAVR® THV System is designed to be a solution for all patients, including both older, younger and less-active patients. Our first in class DurAVR® THV is a single-piece valve with a novel, biomimetic design that aims to replicate the normal blood flow of a healthy human aortic valve as compared to traditional three-piece aortic valves. The DurAVR® THV System has shown restoration of laminar flow similar to individuals with a healthy aortic valve, and early left ventricular reverse remodeling compared with pre-TAVR and similar to healthy controls.

In a pooled analysis of 100 patients derived from our ongoing First-In-Human (“FIH”) study (referred to as the “EMBARK” study) and early feasibility studies (“EFS”) conducted in the United States and Europe, the DurAVR® THV demonstrated single digit mean gradients, large effective orifice areas (“EOAs”), no moderate or severe paravalvular leaks and no valve related mortality, with 97% freedom from prosthesis-patient mismatch (“PPM”). These results were observed in a cohort of small annuli patients similar to the one reported in the SMall Annuli Randomized To Evolut™ or SAPIEN™ Trial (“SMART”), a prospective, multicenter, randomized controlled trial evaluating transcatheter aortic valve performance in patients with small aortic annuli. PPM affects a significant proportion of TAVR patients, particularly patients with a small aortic annulus and has been associated with impaired long-term survival following surgical aortic valve replacement (“SAVR”).

In addition, our DurAVR® THV has been developed with the aim to increase durability and last longer than traditional three-piece designs through the use of our ADAPT® anti-calcification tissue including a molded single-piece of tissue designed to mimic the performance of a pre-disease human aortic valve, which we believe can result in improved hemodynamics as compared to traditional three-piece designs. These designs and features cumulatively aim to provide a better quality of life as compared to the current standard of care associated with traditional three-piece designs. We intend to test these features in the DurAVR® THV randomized, global pivotal study (the “PARADIGM Trial”).

The PARADIGM Trial is a prospective, randomized, controlled multicenter, international study wherein subjects are randomized to receive either a TAVR using the DurAVR® THV or TAVR using a commercially available and approved THV in an ‘All Comers Randomized Cohort.’ The primary end point of the PARADIGM Trial is a composite of all-cause mortality, all stroke and cardiovascular hospitalizations at 1-year post-procedure, according to Valve Academic Research Consortium‑3 (“VARC-3”), a globally accepted consensus framework that standardizes clinical endpoint definitions for aortic valve clinical research. The endpoint will be evaluated as a non-inferiority analysis. We anticipate that the subjects will include a broad array of risk profiles. Subjects with a failed surgical bioprosthesis in need of a ViV TAVR are enrolled in a separate parallel registry.

In 2025, we advanced regulatory activities in Europe, with the goal of securing approval to commence the PARADIGM Trial in a number of European countries. In October 2025, we secured the first European regulatory approval in Denmark and subsequently enrolled and treated the first patients marking the formal initiation of the PARADIGM Trial. In November 2025, we also received Investigational Device Exemption (“IDE”) approval from the FDA for the PARADIGM Trial. The FDA granted a staged approval authorizing enrollment of the first 200 patients. We may request authorization to expand enrollment for the remaining subjects through an IDE supplement. Throughout the year, our cross‑functional teams continued to execute site activation, regulatory preparation, and operational readiness activities in anticipation of regulatory approval in each participating country.

We expect the data from the PARADIGM Trial could provide the clinical evidence required for regulators to approve commercialization. This includes premarket approval that is required for commercialization of the DurAVR® THV System in the United States and CE Mark approval in Europe.

We continued strengthening our operational infrastructure during the year, advancing quality management system buildout to support upcoming clinical activities and future ISO 13485 certification. Key quality procedures and standard operating documents were released to establish the framework for a mature, compliant system and mitigate audit risk. In parallel, manufacturing scale-up activities progressed, including cross-training of inspection personnel, expansion of clean room capacity, and ongoing process development initiatives to ensure robust, high-yield production in line with projected demand.

We are a development stage company and have incurred net losses each year since operation, however, we believe that we have significant growth potential in a large, underpenetrated and growing TAVR market. Since the inception of the TAVR procedure, the annual volume of TAVR procedures in the United States has increased significantly year-over-year, with an estimated 73,000 patients having undergone a TAVR procedure in the United States in 2019 according to the STS/ACC TVT Registry. According to FMI, a market research firm, the total global market opportunity for TAVR in relation to severe aortic stenosis and in relation to ViV procedures is expected to reach $9.9 billion and $2.5 billion, respectively, in 2028.

Our innovation-focused R&D practice is driven by rapid technological advancement and significant input from leading interventional cardiologists and cardiac surgeons. As a company that is primarily in the development phase, we currently generate small amounts of revenue and income which are insufficient to cover our investment in research, development and operational activities resulting in recurring net operating losses, incurred since inception. We, like other development stage medical device companies, experience challenges in implementing our business strategy due to limited resources and a smaller capital base as we prioritize product development, minimize the period to the commencement of commercial sales, ensure our focus on quality as well as scale our operations. The development and commercialization of new medical devices is highly competitive. Those competitors may have substantial market share, substantially greater capital resources and established relationships with the structural heart community, potentially creating barriers to adoption of our technology. Our success will partly be based on our ability to educate the market about the benefits of our disruptive technology including current unmet clinical needs compared to commercially available devices as well as how we plan to capture market share post commercialization.

We are dedicated to developing technological enhancements and new indications for existing products, and less invasive and novel technologies to address unmet patient needs in structural heart disease. That dedication leads to our initiation and participation in clinical trials that seek to prove our pipeline is safe and effective as the demand for clinical and economic evidence remains high.

From time to time, we enter into strategic agreements aimed at enhancing our business operations and profitability. For example, in April 2023, we invested in and entered into a development agreement (the “Development Agreement”) with, v2vmedtech, inc. (“v2vmedtech”), which develops an innovative heart valve repair device for the minimally invasive treatment of mitral and tricuspid valve regurgitation.

Market Opportunity

According to the World Bank, the total population over 65 in the United States and the European Union was approximately 173.6 million as of 2024. According to FMI, the total global market opportunity for TAVR in relation to severe aortic stenosis and in relation to ViV procedures is expected to reach $9.9 billion and $2.5 billion, respectively, in 2028. The key specific markets that our Company is initially targeting are North America and Europe due to these markets accounting for the majority of the above global opportunity. FMI indicated that the North American and European markets averaged 53% and 38% of the global market share, respectively, during the period 2016 to 2023. FMI forecasts that the market opportunity in relation to severe aortic stenosis for North America and Europe will reach $5.5 billion and $3.7 billion, respectively, in 2028; and the market opportunity in relation to ViV procedures is forecast to reach $1.5 billion and $0.8 billion, respectively, in 2028. To calculate these future market values, FMI has relied on actual data from 2023 collated from a variety of published sources and key medical experts and applied a projected CAGR of 14.9% for the global market, 16.2% for the North American market, and 14.0% for the European market. A non-exhaustive list of factors that may impact these forecast calculations include key players’ historic growth; companies and manufacturers working together to develop new, affordable and timesaving technologies; new product launches and approvals; rising demand for THV replacement; availability and cost of products; growing investment in healthcare expenditure; and increased regulatory focus on patient safety and reimbursement policies. In addition, we expect the TAVR market to benefit from general trends, including an aging population, earlier diagnosis of aortic stenosis, increased incidence of obesity and diabetes (which contribute to heart disease), as well as the broader patient populations’ desire to pursue a more active lifestyle.

Since the inception of the TAVR procedure, the annual volume of TAVR procedures in the United States has increased significantly year-over-year, with an estimate of nearly 100,000 patients having undergone a TAVR procedure in the United States in 2022 according to the TVT Registry. We believe that the rising geriatric population and the growing cardiovascular device market provides us with a clear business opportunity. The use of healthcare services is significantly higher among older people.

DurAVR® THV’s single-piece native shaped biomimetic design replicates the performance of a healthy human aortic valve and is designed to restore normal blood flow as compared to traditional three-piece transcatheter valves, either balloon expandable or self-expanding, which do not restore normal aortic flow. We believe this design, in combination with the ADAPT® tissue technology, has the potential to allow the DurAVR® THV to last longer than traditional three-piece aortic valves, which have multiple leaflets sewn together that may lead to compromised durability.

Our Product Candidates

DurAVR® THV, which employs our ADAPT® anti-calcification tissue and is deployed using our ComASUR® Delivery System, is currently in clinical development.

DurAVR® Transcatheter Heart Valve System

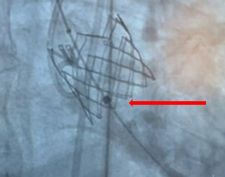

Our DurAVR® THV is a novel transcatheter aortic valve designed in collaboration with the world’s leading interventional cardiologists and cardiac surgeons to treat symptomatic severe aortic stenosis – a potentially life-threatening condition resulting from the narrowing of the aortic valve. The balloon-expandable DurAVR® THV is the first biomimetic valve, shaped to mimic the performance of a healthy human aortic valve and aims to replicate normal aortic blood flow. Our DurAVR® THV is made using a single piece of molded bovine pericardial tissue treated with ADAPT®, our patented anti-calcification tissue technology, sutured inside a cobalt-chromium frame. ADAPT® tissue, which is FDA-cleared, has been used clinically for over 10 years and distributed for use in over 55,000 patients worldwide. The DurAVR® THV System is comprised of the DurAVR® valve, the ADAPT® tissue, and the balloon-expandable ComASUR® Delivery System. These designs and features cumulatively aim to restore a better quality of life compared to the current standard of care associated with traditional three-piece designs. We intend to evaluate the safety and efficacy of the DurAVR® THV against commercially approved TAVR devices in the global pivotal PARADIGM Trial (NCT07194265).

The DurAVR® THV has the following attributes:

•

it is the first transcatheter aortic valve to use a patented construction of a molded single-piece of bioengineered tissue (our ADAPT® anti-calcification tissue with molded leaflets (see “ADAPT® Anti-Calcification Tissue”));

•

it has fewer sutures and seams when compared with conventional valves, thereby preserving tissue integrity with the intent to reduce calcification risk to extend valve durability;

•

it is uniquely shaped to emulate the performance of a healthy human valve and produce long leaflet coaptation, laminar flow and near-normal hemodynamics;

•

it has large open cells in the stent frame to facilitate coronary access; and

•

it utilizes the ComASUR® balloon expandable Delivery System (see “ComASUR® Delivery System”) for controlled deployment and accurate placement.

ADAPT® Anti-Calcification Tissue

The ADAPT® tissue engineering process is an anti-calcification preparation that transforms xenograft tissue (bovine pericardium) into durable bioscaffolds that are used to mimic human tissue for surgical repair in multiple settings, including aortic valve replacement. The outcome of the ADAPT® tissue engineering process is a novel, acellular, biostable and non-calcifying biomaterial.

The ADAPT® tissue engineering process involves multiple steps to transform bovine pericardium into a durable bioprosthetic material. Bovine spongiform encephalopathy-free bovine pericardium is decellularized to remove all cellular antigens that initiate an immune response. The material is then crosslinked to enable maintenance and stabilization of strength and elasticity to improve mechanical resistance. The cytotoxicity is further reduced using detoxification and sterilization processes and anti-calcification methodology to remove and bind aldehydes and enable safe storage in a non-glutaraldehyde solution. Post-implantation, ADAPT® tissue provides a scaffold for cell migration to create the optimal environment. Migrated cells can stimulate site-specific remodeling and repair and enable the formation of new blood vessels.

Our proprietary ADAPT® tissue has been clinically demonstrated to be calcium-free for up to 10 years post-procedure, according to Performance of the ADAPT-Treated CardioCel® Scaffold in Pediatric Patients With Congenital Cardiac Anomalies: Medium to Long-Term Outcomes, published by William Neethling et. al., and it has been distributed for use in over 55,000 patients globally in other indications. Our ComASUR® balloon-expandable Delivery System, which was developed in consultation with physicians, is designed to provide precise alignment with the heart’s native commissures to achieve accurate placement of the DurAVR® THV.

To meet the need for a durable THV, made from ADAPT® tissue scaffold, we have created the DurAVR® THV, which is a first in class, biomimetic single-piece valve with optimal hemodynamic and durability properties. Based on published clinical data in several peer-reviewed journals, including The Journal of Thoracic and Cardiovascular Surgery, the Expert Review of Medical Devices, and Interactive Cardiovascular and Thoracic Surgery, ADAPT® has been observed to offer potentially significant improvements compared with other widely available commercial processes adopted by healthcare providers, including with respect to bio-compatibility, durability, strength, pliability, functionality and controlled remodeling.

ComASUR® Delivery System

Our ComASUR® Delivery System is a physician-developed balloon expandable delivery system that contains a reinforced steerable catheter for a precise deflection through the heart anatomy in a controlled manner to avoid damage to the aorta. This delivery system provides controlled deployment and accurate placement of our DurAVR® THV. Our ComASUR® Delivery System is designed to achieve precise alignment with the heart’s native commissures to achieve ideal valve positioning.

Within the ComASUR® Delivery System, we have rotational control of the DurAVR® valve with the native commissures. This allows for commissure alignment, which is not achieved consistently in competitive delivery systems. Commissure alignment is important because it positions the transcatheter valve leaflets in line with the patient’s native anatomy, supporting optimal hemodynamics, facilitating future coronary access, and enabling consistent device performance. This feature positions the TAVR valve leaflets exactly in line with the anatomical orientation of the recipient’s native valve leaflets. We have a patent pending for this system.

The ComASUR® Delivery System provides even balloon expansion for the accurate placement of the DurAVR® THV as well as ease of use. Under fluoroscopic guidance the physician precisely aligns the DurAVR® THV with the native annulus before deployment in the following manner:

|

First, the balloon starts out as collapsed.

|

|

|

|

|

The balloon is then expanded and the DurAVR® THV is deployed.

|

|

|

|

|

Finally, the balloon is deflated and removed.

|

Clinical Results and Trials

Over 130 patients have been successfully treated with the DurAVR® THV, including de novo (first time) aortic stenosis cases, ViV patients and complex anatomies such as bicuspid aortic valve patients. We continue to expand the level of global experience and build the body of clinical evidence for the DurAVR® THV System through our clinical development program, comprised of the ongoing EMBARK study, EFSs in the United States and European Union (the “U.S. EFS” and “EU EFS,” respectively) and the recently initiated global, pivotal PARADIGM Trial, in addition to compassionate use cases.

The EMBARK study, initiated in November 2021 in Tbilisi, Georgia, has enrolled nine cohorts and demonstrated consistent device performance, favorable hemodynamic outcomes, and an acceptable safety profile through available follow-up periods. In addition, we enrolled 15 patients across four centers in our U.S. EFS, achieving 100% implant success with no mortality, disabling stroke, or life-threatening bleeding at 30 days. Our EU EFS enrolled 15 patients to further evaluate safety and ViV performance in a controlled setting. 30-day data from these studies were pooled and recently published in EuroIntervention. This data demonstrates promising clinical and echocardiographic outcomes in patients with small aortic annuli, a population at greater risk for impaired valve hemodynamics. The overall technical success rate was high at 93% with no deaths, a low stroke rate (2%), single-digit gradients (8.2 mmHg), large EOAs (2.2 cm2), and low rate of moderate or greater prosthesis-patient mismatch (3%) through 30 days.

Building on these clinical programs, in 2025 we initiated our PARADIGM Trial, a global, prospective, randomized, controlled, multicenter study comparing DurAVR® THV to commercially available THVs. The PARADIGM Trial is designed to generate the clinical evidence necessary to support global regulatory approval. The first patients were enrolled in October 2025, and in November 2025, we announced that the FDA granted IDE approval for a staged enrollment for the first 200 patients in the PARADIGM Trial in the United States.

Competition

We compete in the cardiovascular device market, and in particular the TAVR market. These markets are characterized by rapid change resulting from technological advances, innovations and scientific discoveries. Our products face a mix of competitors ranging from large manufacturers with multiple business lines to small manufacturers offering a limited selection of products. In addition, we face competition from providers of other medical therapies, such as pharmaceutical companies. Our primary competitors include Edwards Lifesciences Corporation and Medtronic. Currently, no competitor has a single-piece tissue TAVR commercially available or has publicly disclosed that a single-piece tissue TAVR is in development.

Major shifts in industry market share have occurred in connection with product corrective actions, physician advisories, safety alerts, results of clinical trials to support superiority claims, and publications about products, reflecting the importance of product quality, product efficacy and quality systems in the medical technology industry. In the current environment of managed care, economically motivated customers, consolidation among healthcare providers, increased competition, declining reimbursement rates, and national and provincial tender pricing, competitively priced product offerings are essential to our business. In order to compete effectively, we must continue to create or acquire advanced technology, incorporate this technology into proprietary products, obtain regulatory approvals in a timely manner, maintain high-quality manufacturing processes, and successfully market these products.

Intellectual Property

We rely on a combination of patent, copyright, trademark and trade secret laws and confidentiality and invention assignment agreements to protect our intellectual property rights in the United States and other markets. United States federal registrations for trademarks can remain in force in perpetuity, provided the mark is still being used in commerce and the maintenance/renewal filings are made as required by the sixth year after registration, by the tenth year after registration, and every ten years thereafter.

As of December 31, 2025, Anteris owned a total of 47 active patents expiring between 2032 and 2045, and 75 pending patent applications, as further detailed below.

In the category of prosthetic heart valve devices, we are the sole owner of eight active United States patents, seven pending United States patent applications, seven active Australian patents, three pending Australian patent applications, eight active patents in other countries, and 31 pending applications in other countries. These patents and pending applications are directed to features that are expected to provide competitive advantages such as: a novel process for production of calcification resistant cross-linked biomaterials for the prosthetic valve; three-dimensional molded heart valve leaflets made of cross-linked biomaterial that mimic the performance of a native heart valve designed to provide enhanced performance characteristics such as low mean pressure gradient, low leaflet stress, large open area, high coaptation area and high duration in an open state, to name a few; a prosthetic heart valve that has localized protective covering members that prevent direct contact between the valve and the stent frame to enhance the durability and longevity of the prosthetic valve when the valve is in an open state; and attachment of the biomaterial valve to the stent frame in a novel manner that reduces stresses on the biomaterial of the prosthetic valve.

In the category of delivery systems for the prosthetic heart valve devices, we are the sole owner of three active United States patents, seven pending United States patent applications, one active Australian patent, three pending Australian patent applications, two pending PCT applications, one active patent in other countries, and 15 pending applications in other countries. These patents and pending applications are directed to features that are expected to provide competitive advantages such as: controllable and predictable commissural alignment; a balloon folding technique that mitigates valve rotations during expansion; a single-use valve crimping device; and a delivery catheter hard stop member made of a braided metal material that provides improved trackability, effective expansion of the delivery sheath during advancement, and increased longitudinal compressive strength that serves to maintain the longitudinal position of the prosthetic heart valve on the balloon member.

In the category of sterilization and storage of the prosthetic heart valve devices, we are the sole owner of two active United States patents, one active Australian patent, seven active patents in other countries, and one pending application in other countries. These patents and pending applications are directed to features that are expected to provide competitive advantages such as a novel process for sterilizing the valve made of collagen-containing implantable biomaterials and storage thereafter.

In the category of packaging, we are the sole owners of two active United States patents, one pending United States patent application, two active Australian patents, one pending Australian patent application, five active patents in other countries, and four pending patent applications in other countries. These patents and pending applications are directed to features that are expected to provide competitive advantages such as a packaging design that includes integrated components and mechanisms for preparing and mounting the valve on the delivery catheter system to make the clinician’s valve preparation process more efficient and user-friendly.

Anteris holds a 30% interest in v2vmedtech. v2vmedtech’s intellectual property is directed to implantable medical devices for mitigating heart valve regurgitation. Using a transcatheter deployment technique, one or more clip devices are attached to the leaflets of a patient’s mitral or tricuspid heart valve to permanently join together edge portions of the leaflets. This is often referred to as an edge-to-edge repair procedure. As of December 31, 2025, v2vmedtech had 13 pending patent applications and is the exclusive licensee of two pending patent applications owned by Columbia University.

We have trademark registrations for several of our most material marks, including “ADAPT,” “ADAPT FOR LIFE”, “ANTERIS”, “ComASUR”, “DurAVR”, and “GYNECEL”. Our filing for the “ANTERIS” trademark in India is pending. Our trademarks were obtained between 2006 and 2024. Nearly all of our United States trademarks are federal trademarks.

We operate in an industry characterized by extensive patent litigation. Patent litigation may result in significant damage awards and injunctions that could prevent the manufacture and sale of affected products or result in significant royalty payments in order to continue selling the products.

We undertake reasonable measures to protect our patent rights, including monitoring the products of our competitors for possible infringement of our patents. Protecting our intellectual property rights is important to us, and we plan to continue to maintain and defend our rights regarding our intellectual property.

License Agreements

4C Medical Technologies

On August 30, 2017, and as further amended, we entered into a supply and license agreement (as amended, the “4C Agreement”) with 4C Medical Technologies, Inc. (“4C”), a medical technology company that develops medical devices for the treatment of cardiovascular valve disease. Under the terms of the 4C Agreement, we supply and sell ADAPT® tissue to 4C, to be used in 4C’s production of medical devices related to mitral valves and tricuspid human heart valves and granted a limited license to our related sterilization methods only in connection with use of ADAPT® tissue by 4C in its production of medical devices.

Sales under the 4C Agreement are made pursuant to individual purchase orders at a price per unit based on anticipated annual volume. There are no minimum purchase commitments under the 4C Agreement.

During the term of the 4C Agreement, our supply of ADAPT® tissue to 4C is exclusive, meaning that we agree not to develop, manufacture, or sell certain ADAPT® tissue-based products in the mitral valve or tricuspid valve field other than for 4C without prior written approval. We have received $10.2 million in proceeds through December 31, 2025 (life to date) under the 4C Agreement relating to the sale and supply of ADAPT® tissue-based products to 4C and granting 4C a worldwide license to use our sterilization method in connection with those supplied ADAPT® tissue-based products.

Pursuant to the 4C Agreement, 4C was granted a limited, revocable and royalty free license to use certain of our trademarks for marketing purposes for 4C’s medical devices that use ADAPT® tissue. On October 14, 2019, in light of the transaction with LeMaitre, we revoked 4C’s license to the CardioCel™ trademark only. We retained our intellectual property rights existing at the time of the 4C Agreement (except for limited licenses granted to 4C in effect during the term of the 4C Agreement), including new intellectual property rights relating to our tissue products developed either solely by us or jointly by us and 4C. The last-to-expire patent related to the intellectual property covered by the 4C Agreement is scheduled to expire in 2032.

The 4C Agreement had an initial term that expired on June 1, 2025, and under its terms would automatically renew for successive one-year periods unless either party provided written notice of non-renewal at least 180 days prior to the applicable renewal date. On November 26, 2025, we notified 4C that we would not renew the 4C Agreement for the next renewal term. We will not incur any early termination penalties in connection with its non-renewal of the 4C Agreement. The termination of this contract does not materially impact our financial results.

Collaborations

v2vmedtech

On April 18, 2023, we purchased 30% of the equity capital stock of v2vmedtech, pursuant to a contribution and stock purchase agreement (the “Stock Purchase Agreement”), and concurrently contributed $0.2 million and entered into a series of agreements (collectively, the “v2v Agreements”) with v2vmedtech. v2vmedtech has a license agreement with Columbia University to develop an innovative heart valve repair device utilizing a transcatheter edge-to-edge repair method for a minimally invasive treatment of mitral and tricuspid valve regurgitation, also known as leaky valve.

Under the terms of the v2v Agreements, we agreed to provide certain development services to v2vmedtech in exchange for equity in v2vmedtech. Pursuant to the v2v Agreements, we provide engineering, clinical, regulatory, marketing, and executive management resources, but excluding medical and chief medical officer services, in connection with v2vmedtech’s development of these valve repair devices. We are responsible for developing products and preparing regulatory filings and all costs and expenses incurred by us directly, related to the development of devices constitute development contributions under the v2v Agreements, for which we are solely responsible. These contributions are to be provided over five stages linked to key development and regulatory requirements for the device for transcatheter edge-to-edge repair of the mitral valve (“TEER Product”).

Stage 1 is the development of a preferred concept for the TEER Product, during which we will provide analytical, engineering and product development services for the TEER product, gather and document preliminary or critical product requirements, create product specifications, design at least one concept to meet that product specification, and provide initial prototypes. During this stage, v2vmedtech will also establish a separate medical advisory board (the “v2v Advisory Board”). Stage 1 concluded with a design review with non-Anteris members of v2vmedtech, prior to proceeding to Stage 2. The R&D contributions (excluding general and administration expenses) paid by us under Stage 1 were $2.2 million.

Stage 2 involved manufacturing and testing prototypes of the preferred concept to finalize the TEER Product design for concept lock. This stage included additional engineering and product development services to modify the preferred concept of the TEER Product at our sole discretion. Before we make a decision to advance to Stage 3, a design review with non-Anteris members of v2vmedtech will be conducted and their feedback will be considered. In addition, to advance to Stage 3, the TEER Product must meet all established criteria in our quality system. The R&D contributions (excluding general and administration expenses) paid by us as set out in the Development Agreement under Stage 2 are expected to be $0.4 million to $0.8 million.

Stage 3 involves non-clinical bench lab testing of the TEER Product, at our discretion. Before we make a decision to advance to Stage 4, a design review with non-Anteris members of v2vmedtech will be conducted and their feedback will be considered. The R&D contributions (excluding general and administration expenses) paid by us as set out in the Development Agreement under Stage 3 are expected to be $0.8 million to $1.8 million.

Stage 4 involves preclinical acute and chronic studies of the TEER Product in animals to support regulatory submissions, which will be undertaken at our discretion. Before we make a decision to advance to Stage 5, a design review with non-Anteris members of v2vmedtech will be conducted and their feedback will be considered. Approval from v2vmedtech’s Advisory Board may be required before proceeding to Stage 5. The R&D contributions (excluding general and administration expenses) paid by us as set out in the Development Agreement under Stage 4 are expected to be $0.7 million to $1.6 million.

Stage 5 is the first use of the TEER Product in a first-in-human study in one cohort of patients anywhere in the world. During this stage, v2vmedtech will enter into agreements with the sites and practitioners performing the first-in-human study services and must maintain appropriate insurance. A review of endpoints and resulting data from the first-in-human study will be conducted by us and by appropriate non-Anteris members of v2vmedtech in order to determine the success of the first-in-human study. The R&D contributions (excluding general and administration expenses) paid by us under Stage 5 as set out in the Development Agreement are expected to be $1.0 million to $2.2 million.

During Stages 2 through 5, we may solicit input from the v2v Advisory Board and will coordinate, facilitate and participate in meetings of the v2v Advisory Board. We are generally permitted to use our own employees, resources, lab facilities and other internal resources during the five development stages.

We have an option to terminate our activities for v2vmedtech, subject to certain break rights. These break rights allow us to discontinue additional development contributions subject to a fee of $0.2 million during Stage 1 and incrementally increasing by $0.2 million for each stage of development to a maximum $1.0 million break fee in Stage 5. We will also pay all customary corporate, operational, and legal costs (“operational contributions”) of v2vmedtech up to an annual amount determined by vmedtech’s board of directors. After the earlier of the completion of Stage 5 or the incurrence of $10.0 million of development contributions and operational contributions, our ownership stake in v2vmedtech will be increased from 30% to between 58% and 60%.

v2vmedtech owns all intellectual property rights to the technology and data developed (the “Developed Technology and Data”) pursuant to the v2v Agreements. However, under the terms of the v2v Agreements, v2vmedtech grants us a perpetual and exclusive license to the Developed Technology and Data for medical device applications other than leaky valve devices. As v2vmedtech is a development company, there is no revenue currently generated by this entity.

The v2v Agreements will expire one year after completion of Stage 5. We may terminate the v2v Agreements upon exercise of our break rights under the Stock Purchase Agreement and payment of the applicable break fee or upon a material breach by v2vmedtech. v2vmedtech may terminate the v2v Agreements once we no longer own any shares of v2vmedtech’s issued and outstanding capital stock or upon its exercise of its break rights under the Stock Purchase Agreement or the exercise of certain rights it holds under the Stock Purchase Agreement. We and v2vmedtech may terminate the v2v Agreements upon an event of insolvency or a material breach by the other party.

Development is currently in Stage 2 and has reached concept lock on the clips and coupler. Timing for a FIH trial cannot be reasonably determined at this time as it is contingent on successful completion of further stages of R&D, including the design, prototyping and testing, preclinical testing and completion of regulatory submissions. The timing to complete these activities is influenced by the v2v Agreements, which state that the development agreement can be terminated if certain expenditure amounts, development milestones or regulatory approvals are not incurred or achieved from March 31, 2027 and onwards. The total amount of eligible development contributions and operational contributions paid by us under the v2v Agreements as of December 31, 2025 was $6.2 million.

Single Source Suppliers

Aran Biomedical

We are party to a supply and quality agreement (the “Aran Supply Agreement”), dated November 16, 2021, with Aran Biomedical Teoranta (“Aran”) (subsequently acquired by Integer Holdings Corporation) pursuant to which Aran supplies us with certain knitted materials from time to time pursuant to one or more purchase orders and in accordance with reasonable quality requirements provided by us. The Aran Supply Agreement has an initial term of five years and renews thereafter for successive one-year terms upon mutual written agreement of the parties. Either us or Aran may terminate the Aran Supply Agreement upon an uncured material breach.

Harvey Industries Group

We have entered into a supply and quality agreement (the “Harvey Supply Agreement”) with Harvey Industries Group Pty Ltd (“Harvey”), a supplier of animal derived materials for therapeutic applications. Under the Harvey Supply Agreement, Harvey supplies us with bovine pericardia used in the manufacturing of our products pursuant to orders placed by us. We have the ability to reject any product that does not meet the applicable specifications. The Harvey Supply Agreement expires in May 2026 but may be extended by mutual agreement between us and Harvey. If the Harvey Supply Agreement is not extended, Harvey will continue to supply us with bovine pericardia for an additional four months after the expiration of the Harvey Supply Agreement upon our request. We may terminate the Harvey Supply Agreement without cause upon 90 days written notice, and Harvey may terminate the Harvey Supply Agreement with 12 months written notice. Either us or Harvey may terminate the Harvey Supply Agreement for cause upon an uncured breach or a non-remediable breach.

NPX Medical

We are party to a services agreement (the “NPX Services Agreement”), dated March 25, 2020, and subsequently amended on February 21, 2021 and March 24, 2024, with NPX Medical, LLC (“NPX”), pursuant to which NPX provides certain engineering and manufacturing services to us as requested by us in purchase orders from time to time. NPX also provides certain product development services to us under the NPX Services Agreement. The NPX Services Agreement had an original expiration date of March 25, 2021 and renews automatically for successive one-year terms unless terminated. Either party to the NPX Services Agreement may terminate the agreement without cause upon 30 days written notice to the other party or for cause upon an uncured material breach of the NPX Services Agreement.

We are also party to a quality agreement with NPX (the “NPX Quality Agreement”), dated February 11, 2021, which provides for certain quality requirements for the products manufactured for us by NPX, as specified by us in purchase orders made under the NPX Services Agreement. The NPX Quality Agreement will remain in effect as long as the NPX Services Agreement is in effect.

Switchback Medical

On July 28, 2025, we entered into the First Amended and Restated Master Services Agreement (the “A&R MSA”) with Switchback Medical, LLC (“Switchback”), pursuant to which Switchback provides various development and manufacturing services, including engineering and testing services, pursuant to purchase orders made by us from time to time, at set prices per unit, and in compliance with various quality management and regulatory requirements.

Under the A&R MSA, we granted Switchback a limited, exclusive, revocable, non-sublicensable, fully paid-up, royalty-free license to certain of our intellectual property to be used solely for the purpose of manufacturing products during the term of the A&R MSA. We retain all rights, title and interest in the results of any testing services, reports or data generated or provided by Switchback and to any developed intellectual property.

The A&R MSA expires on March 31, 2028, and will automatically renew for successive one-year terms unless terminated by either the party at least 180 days prior to the end of the then-current renewal term.

Taurus Engineering and Manufacturing

We are party to a supplier quality agreement (the “Taurus Supplier Agreement”), dated February 15, 2024, with Taurus Engineering and Manufacturing, Inc. (“Taurus”), under which Taurus provides us with certain manufacturing services and supplies us with raw materials in accordance with specified quality requirements and other specifications. Taurus is not an exclusive supplier to us for the materials that it supplies, but under the terms of the Taurus Supplier Agreement, Taurus may not supply anyone other than us with the materials covered by the Taurus Supplier Agreement. The Taurus Supplier Quality Agreement had an initial two‑year

term that ended on February 15, 2026. Arrangements are ongoing to extend

the agreement in relation to quality and supply.

Other Agreements

CRF

We are party to a Combined Bioinformatics Master Services Agreement, dated September 1, 2021, with CRF (the “CRF MSA”). Pursuant to the CRF MSA, CRF is engaged on a per project basis to perform independent analyses and provide interpretations on various types of medical data and information, provide comprehensive data coordination and analysis center (“DCAC”) services, manage clinical events and data monitoring committees, and health economics and outcomes research (“HEOR”). Data and other research and results generated or produced by CRF concerning core lab and HEOR activities pursuant to the CRF MSA is jointly owned by us and CRF. The data and other research and results generated or produced by CRF concerning DCAC activities pursuant to the CRF MSA is owned by us. Payment terms under the CRF MSA are set forth in work orders for discrete tasks. The original term of the CRF MSA was through December 31, 2022, and has automatically renewed for subsequent annual terms, with the current term expiring on December 31, 2026. Either party to the CRF MSA may provide notice of termination of the CRF MSA for the subsequent annual period or upon 60 days’ notice.

QMED

We have agreed to be bound by General Terms and Conditions with QMED Consulting A/S (“QMED”), pursuant to which QMED provides certain services to us in accordance with individual service agreements (the “Service Agreements”). Pursuant to the Service Agreements first entered into on July 8, 2024, QMED has agreed to provide us with clinical trial submission support for the EU, including the provision of life science services in the areas of regulatory affairs, training, quality assurance and control, clinical trial consultancy and legal representation. Payment terms and term lengths for discrete tasks and services are set forth in individual Service Agreements. Under the General Terms and Conditions, we may terminate the Service Agreements at our discretion by providing 30 days’ notice, or upon ten days’ notice and payment of a 15% termination fee. Either we or QMED may terminate the Service Agreements upon default or an uncured material breach.

Bright Research

We are party to a Master Services Agreement, dated January 12, 2026 (the “Bright MSA”), with Bright Research Partners, Inc. (“Bright Research”), pursuant to which Bright Research provides services to us in support of various clinical activities identified in applicable statements of work (each, a “SOW”). The Bright MSA has an initial term of five years, however, if any SOWs remain in effect at the end of the term, the agreement will automatically be extended for an additional one-year period, unless earlier terminated. Either party may terminate the Bright MSA, for any reason or for no reason, upon ninety (90) days’ written notice to the other party. The Bright MSA may also be terminated upon an uncured material breach or upon the occurrence of certain insolvency‑related events affecting a party. If a SOW with total fees greater than $1 million is subject to an early termination by us without cause, by Bright Research for cause, or as a result of a change of control, we are required to pay Bright Research an amount equal to 20% of the estimated remaining SOW budget.

Government Regulation

United States FDA Regulation of Medical Devices

Our products are regulated as medical devices in the United States. Accordingly, our products and operations are subject to extensive and ongoing regulation by the FDA under the Federal Food, Drug, and Cosmetic Act (“FDCA”), as well as under other federal, state and local regulatory authorities in the United States. For devices intended for commercial distribution in the United States, the FDA regulates product design and development, preclinical and clinical testing, manufacturing, packaging, labeling, storage, record keeping and reporting, clearance or approval, marketing, distribution, promotion, import and export, and post-marketing surveillance to assure their safety and effectiveness for their intended uses.

Unless an exemption applies, each new medical device we seek to commercially distribute in the United States will require either a premarket notification to the FDA requesting a Section 510(k) clearance, de novo classification, or premarket approval application (“PMA”). Additionally, each significant modification to a 510(k)-cleared or de novo classified device will require a new submission prior to marketing, and each modification that affects the safety and effectiveness of a device with an approved PMA will require a new PMA or supplement. The 510(k) clearance, de novo classification and premarket approval processes can be resource intensive, expensive, and lengthy, and require payment of significant user fees unless a waiver or exemption is available.

FDA classifies medical devices into one of three classes - Class I, Class II or Class III - depending on the degree of risk associated with each medical device and the extent of control needed to provide reasonable assurances with respect to safety and effectiveness.

Class I devices are those for which safety and effectiveness can be reasonably assured by adherence to the FDA’s general controls for medical devices, which include compliance with the applicable portions of FDA’s current good manufacturing practices for devices, establishment registration and device listing, reporting of adverse events and malfunctions, reporting of corrections and removals, and appropriate, truthful and non-misleading labeling and promotional materials. Some Class I devices, called Class I reserved devices, also require premarket clearance by the FDA through the 510(k) premarket notification process described below. Most Class I devices are exempt from the premarket notification requirements. A class I device is not exempt from 510(k) notification requirements if it is intended for a use of substantial importance in preventing impairment of health, or presents a potential unreasonable risk of illness or injury.

Class II devices are those that are subject to the FDA’s general controls and any other special controls deemed necessary by the FDA to ensure the safety and effectiveness of the device. These special controls can include performance standards, patient registries, product-specific FDA guidance documents, special labeling requirements and post-market surveillance. Most Class II devices are subject to premarket review and clearance by the FDA through the 510(k) premarket notification process, although some Class II devices are exempt from such requirement.

Under the 510(k) premarket notification process, a medical device manufacturer provides the FDA with a premarket notification that it intends to begin commercializing a product and demonstrates to the FDA that the product is substantially equivalent to another legally marketed predicate device. To be found substantially equivalent to a predicate device, the device must be for the same intended use and have either the same technological characteristics as the predicate or different technological characteristics that do not raise different questions of safety or effectiveness. In some cases, the submission must include data from clinical studies in order to demonstrate substantial equivalence to a predicate device. Commercialization may commence when the FDA issues a clearance letter finding such substantial equivalence.

Class III devices include those devices that (i) cannot be classified into Class I or Class II because insufficient information exists to determine that general and special controls would provide a reasonable assurance of safety and effectiveness, and (ii) are intended for uses that are life-supporting, life-sustaining, of substantial importance in preventing impairment in human health, or present a potential unreasonable risk of illness or injury.

Additionally, novel devices that lack a predicate device to which they can demonstrate substantial equivalence via the 510(k) premarket notification process are automatically classified into Class III, unless the manufacturer can demonstrate that the device should be classified into Class I or II via the de novo classification process, discussed below. Devices placed in Class III are subject to premarket approval, which requires submission of valid scientific evidence demonstrating a reasonable assurance of the safety and effectiveness of the device for its intended use. The premarket approval process is generally more costly and time consuming than the 510(k) premarket notification process or the de novo classification process. A PMA typically includes, but is not limited to, extensive technical information regarding device design and development, preclinical and clinical trial data, manufacturing information, labeling, and financial disclosure information for the clinical investigators in device studies.

CardioCel™, VascuCel™ and ADAPT® are pericardial tissue products and are Class II medical devices.

CardioCel™ was cleared for marketing by the FDA on January 30, 2014 as a Class II device. A modified version of CardioCel™ was cleared for marketing by the FDA on April 28, 2017. VascuCel™ (another modified version of CardioCel™) was cleared for marketing by the FDA on October 14, 2016. ADAPT® tissue was cleared for marketing by the FDA on April 3, 2020.

Replacement heart valves, including the DurAVR® THV, are Class III medical devices. Additionally, because the ComASUR® Delivery System is required for use of the DurAVR® THV, the ComASUR® Delivery System will be regulated as a component of the DurAVR® THV Class III device (as part of the overall system). Accordingly, the ComASUR® Delivery System will be reviewed under any PMA submitted for the DurAVR® THV System.