Exhibit 99.1

July 29, 2025

Constellium Reports Second Quarter and First Half 2025 Results; Raises Full Year 2025 Guidance

Paris - Constellium SE (NYSE: CSTM) ("Constellium" or the "Company") today reported results for the second quarter and the

first half ended June 30, 2025.

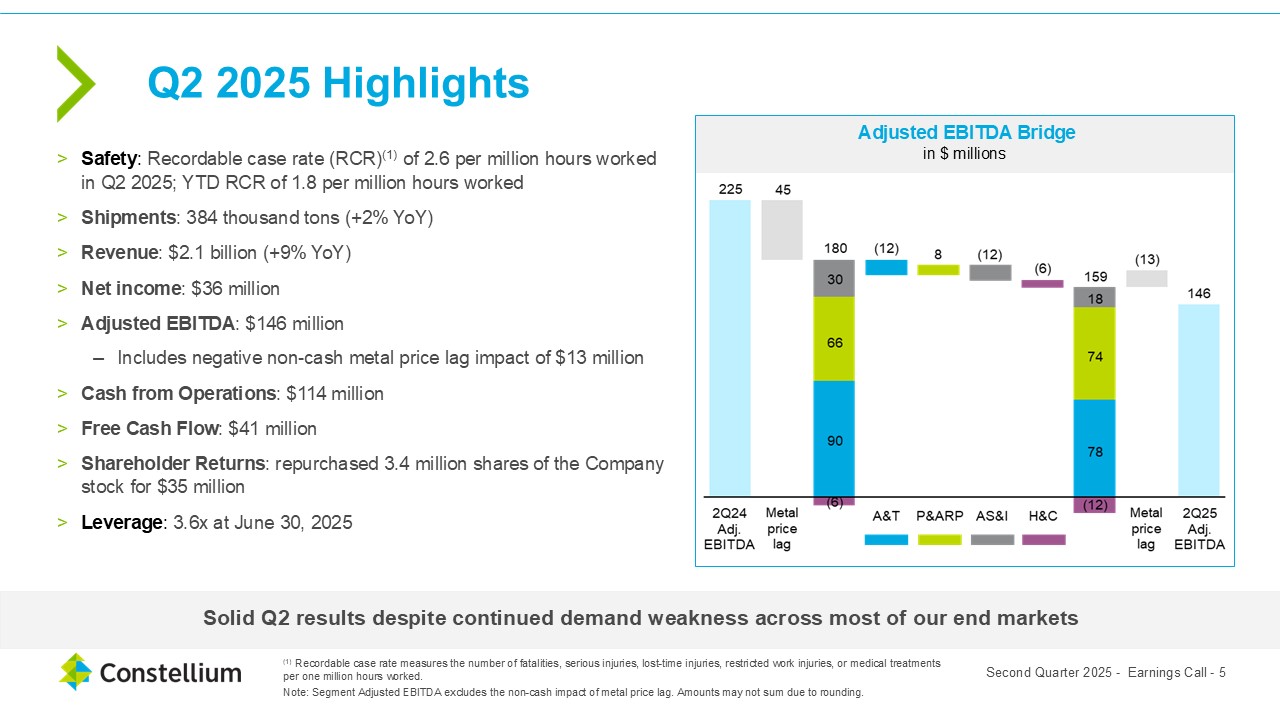

Second quarter 2025 highlights:

| • |

Shipments of 384 thousand metric tons, up 2% compared to Q2 2024

|

| • |

Revenue of $2.1 billion, up 9% compared to Q2 2024

|

| • |

Net income of $36 million compared to net income of $77 million in Q2 2024

|

| • |

Adjusted EBITDA of $146 million

|

> Includes negative non-cash metal price lag impact of $13 million

| • |

Segment Adjusted EBITDA of $78 million at A&T, $74 million at P&ARP, $18 million at AS&I, and $(12) million at H&C

|

| • |

Cash from Operations of $114 million and Free Cash Flow of $41 million

|

| • |

Repurchased 3.4 million shares of the Company stock for $35 million

|

First half 2025 highlights:

| • |

Shipments of 756 thousand metric tons, stable compared to H1 2024

|

| • |

Revenue of $4.1 billion, up 7% compared to H1 2024

|

| • |

Net income of $74 million compared to net income of $99 million in H1 2024

|

| • |

Adjusted EBITDA of $332 million

|

> Includes positive non-cash metal price lag impact of $33 million

| Media Contacts | |

|

Investor Relations

|

Communications

|

|

Jason Hershiser

|

Delphine Dahan-Kocher

|

|

Phone: +1 443 988-0600

|

Phone: +1 443 420 7860

|

|

investor-relations@constellium.com

|

delphine.dahan-kocher@constellium.com

|

1

| • |

Segment Adjusted EBITDA of $153 million at A&T, $135 million at P&ARP, $34 million at AS&I, and $(23) million at H&C

|

| • |

Cash from Operations of $172 million and Free Cash Flow of $38 million

|

| • |

Repurchased 4.8 million shares of the Company stock for $50 million

|

| • |

Leverage of 3.6x at June 30, 2025

|

Jean-Marc Germain, Constellium’s Chief Executive Officer said, “Constellium delivered solid results in the second quarter despite continued demand weakness across most of our end markets outside of packaging. As I

said last quarter, I am proud of our team for their relentless focus on cost reduction efforts and commercial and capital discipline in this uncertain environment. Free Cash Flow was strong at $41 million in the quarter. We repurchased 3.4

million shares for $35 million during the quarter, and we ended the quarter with leverage at 3.6x. We expect this to be the peak for leverage and to trend down as we move through the rest of the year.”

Mr. Germain concluded, “While the tariff and international trade situation remains fluid, given our solid performance in the first half and based on our current outlook, we are raising our guidance for 2025 and now

expect Adjusted EBITDA to be in the range of $620 million to $650 million, excluding the non-cash impact of metal price lag, and Free Cash Flow in excess of $120 million. Our guidance assumes that the overall macroeconomic and end market

environment will remain relatively stable. We also remain confident in our ability to deliver on our long-term target of Adjusted EBITDA of $900 million, excluding the non-cash impact of metal price lag, and Free Cash Flow of $300 million, in

2028. We will continue to closely monitor the situation and update our guidance as necessary. Our focus remains on executing our strategy, driving operational performance, generating Free Cash Flow and increasing shareholder value.”

|

2 |

|

Q2 2025

|

Q2 2024

|

Var.

|

YTD

2025

|

YTD

2024

|

Var.

|

||||||||||||||||

|

Shipments (k metric tons)

|

384

|

378

|

2

|

% |

756

|

758

|

0

|

%

|

|||||||||||||

|

Revenue ($ millions)

|

2,103

|

1,932

|

9

|

%

|

4,082

|

3,812

|

7

|

%

|

|||||||||||||

|

Net income ($ millions)

|

36

|

77

|

(53)

|

%

|

|

74

|

99

|

(25)

|

%

|

||||||||||||

|

Adjusted EBITDA ($ millions)

|

146

|

225

|

n.m.

|

332

|

371

|

n.m.

|

|||||||||||||||

|

Metal price lag (non-cash) ($ millions)

|

(13

|

) |

45

|

n.m.

|

33

|

31

|

n.m.

|

The difference between the sum of reported segment revenue and total group revenue includes revenue from certain non-core activities and inter-segment eliminations. The difference between the

sum of reported Segment Adjusted EBITDA and the Group Adjusted EBITDA is related to Holdings and Corporate and the non-cash impact of metal price lag.

For the second quarter of 2025, shipments of 384 thousand metric tons increased 2% compared to the second quarter of 2024 due to higher shipments in the P&ARP segment, partially offset by lower shipments in the

A&T and AS&I segments. Revenue of $2.1 billion increased 9% compared to the second quarter of the prior year primarily due to higher shipments, favorable sales price and mix, including higher metal prices, and favorable foreign exchange

translation. Net income of $36 million decreased $41 million compared to net income of $77 million in the second quarter of 2024. Adjusted EBITDA of $146 million decreased $79 million compared to Adjusted EBITDA of $225 million in the second

quarter of last year primarily due to an unfavorable change in the non-cash metal price lag impact and weaker results in our A&T, AS&I and H&C segments. This was partially offset by stronger results in our P&ARP segment and

favorable foreign exchange translation.

For the first half of 2025, shipments of 756 thousand metric tons were stable compared to the first half of 2024 due to higher shipments in the P&ARP segment offset by lower shipments in the A&T and

AS&I segments. Revenue of $4.1 billion increased 7% compared to the first half of 2024 primarily due to favorable sales price and mix, including higher metal prices. Net income of $74 million decreased $25 million compared to net income of

$99 million in the first half of 2024. Adjusted EBITDA of $332 million decreased $39 million compared to the first half of 2024 due to weaker results in our A&T, AS&I and H&C segments, partially offset by stronger results in our

P&ARP segment.

|

3 |

Results by Segment

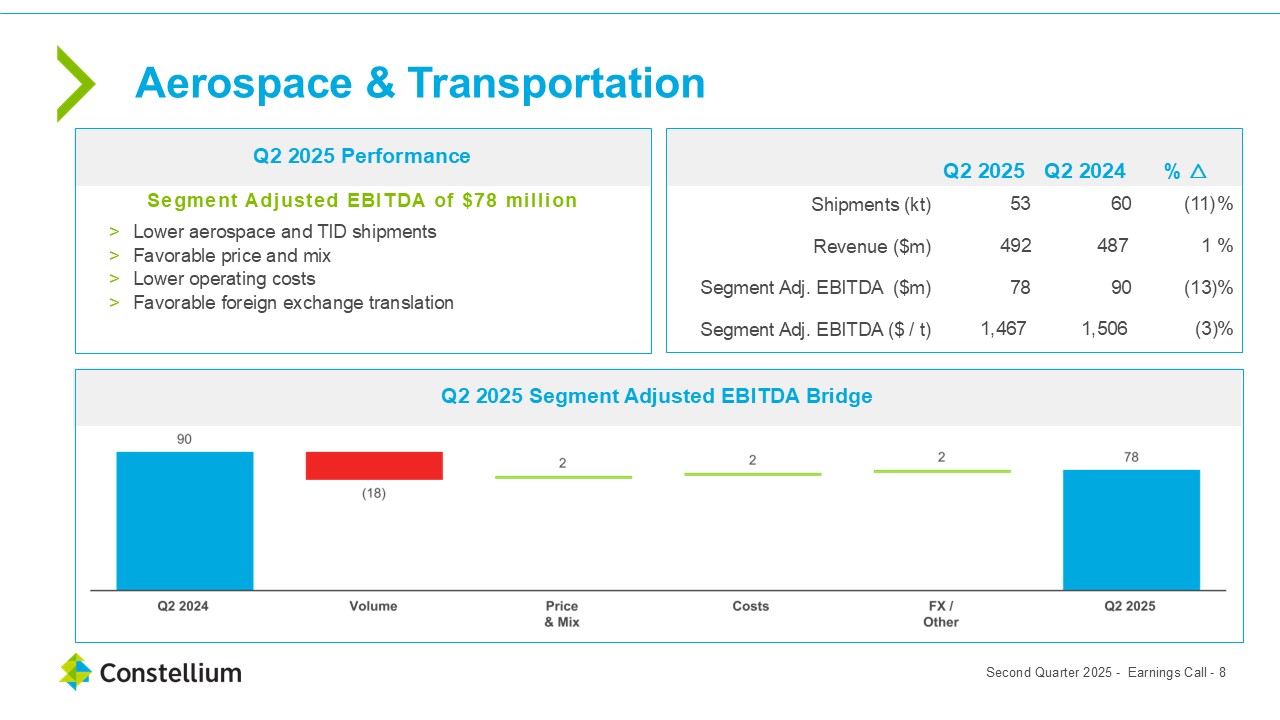

Aerospace & Transportation (A&T)

|

Q2 2025

|

Q2 2024

|

Var.

|

YTD

2025

|

YTD

2024

|

Var.

|

|||||||||||||||||||

|

Shipments (k metric tons)

|

53

|

60

|

(11)

|

%

|

104

|

117

|

(11)

|

%

|

||||||||||||||||

|

Revenue ($ millions)

|

492

|

487

|

1

|

%

|

960

|

966

|

(1)

|

%

|

||||||||||||||||

|

Segment Adjusted EBITDA ($ millions)

|

78

|

90

|

(13)

|

%

|

153

|

177

|

(14)

|

%

|

||||||||||||||||

|

Segment Adjusted EBITDA per metric ton ($)

|

1,467

|

1,506

|

(3)

|

%

|

1,468

|

1,511

|

(3)

|

%

|

||||||||||||||||

For the second quarter of 2025, Segment Adjusted EBITDA of $78 million decreased 13% compared to the second quarter of 2024 primarily due to lower shipments, partially offset by favorable price and mix, lower

operating costs and favorable foreign exchange translation. Shipments of 53 thousand metric tons decreased 11% compared to the second quarter of 2024 due to lower shipments of aerospace and transportation, industry and defense (TID) rolled

products. Revenue of $492 million increased 1% compared to the second quarter of 2024 primarily due to favorable sales price and mix, including higher metal prices, and favorable foreign exchange translation, mostly offset by lower shipments.

For the first half of 2025, Segment Adjusted EBITDA of $153 million decreased 14% compared to the first half of 2024 primarily due to lower shipments and unfavorable price and mix, partially offset by lower

operating costs. Shipments of 104 thousand metric tons decreased 11% compared to the first half of 2024 due to lower shipments of aerospace and TID rolled products. Revenue of $960 million decreased 1% compared to the first half of 2024 primarily

due to lower shipments, mostly offset by favorable sales price and mix, including higher metal prices.

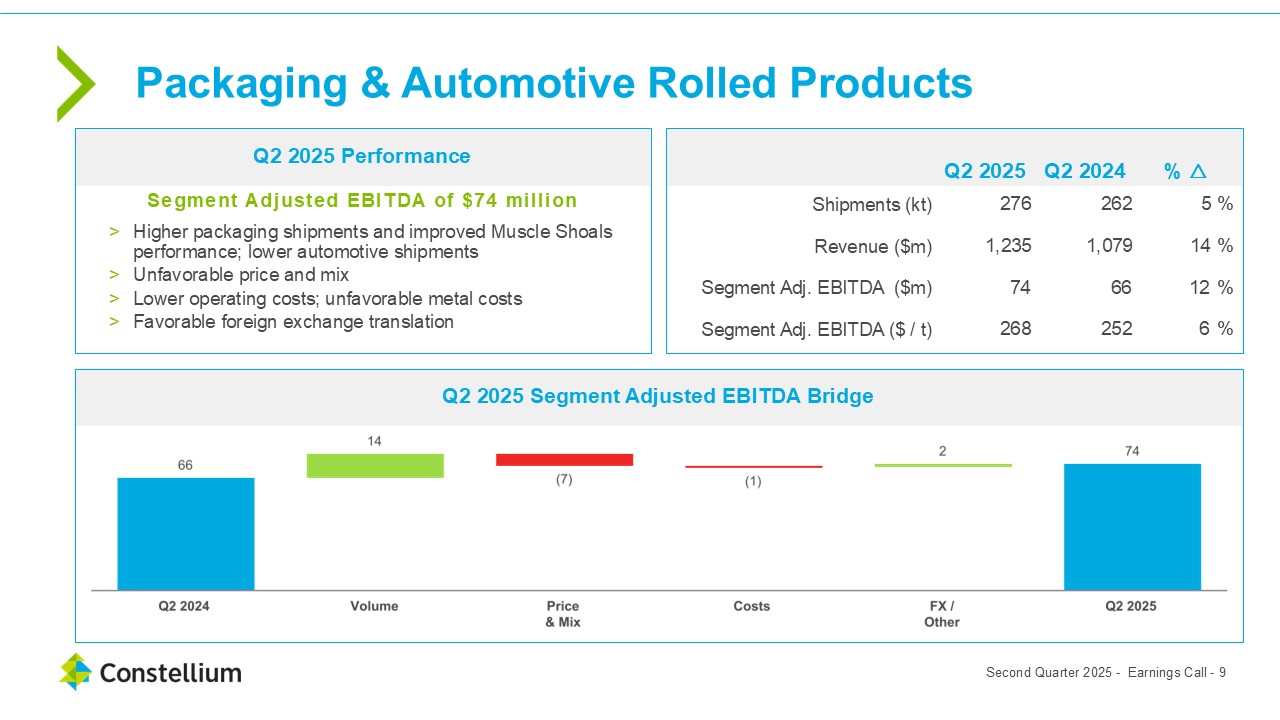

Packaging & Automotive Rolled Products (P&ARP)

|

Q2 2025

|

Q2 2024

|

Var.

|

YTD 2025

|

YTD 2024

|

Var.

|

|||||||||||||||||||

|

Shipments (k metric tons)

|

276

|

262

|

5

|

%

|

545

|

526

|

4

|

%

|

||||||||||||||||

|

Revenue ($ millions)

|

1,235

|

1,079

|

14

|

%

|

2,422

|

2,097

|

15

|

%

|

||||||||||||||||

|

Segment Adjusted EBITDA ($ millions)

|

74

|

66

|

12

|

%

|

135

|

114

|

18

|

%

|

||||||||||||||||

|

Segment Adjusted EBITDA per metric ton ($)

|

268

|

252

|

6

|

%

|

248

|

217

|

14

|

%

|

||||||||||||||||

|

4 |

For the second quarter of 2025, Segment Adjusted EBITDA of $74 million increased 12% compared to the second quarter of 2024 primarily due to higher shipments and improved Muscle Shoals performance, lower operating

costs and favorable foreign exchange translation, partially offset by unfavorable price and mix and unfavorable metal costs. Shipments of 276 thousand metric tons increased 5% compared to the second quarter of 2024 due to higher shipments of

packaging rolled products, partially offset by lower shipments of automotive rolled products. Revenue of $1.2 billion increased 14% compared to the second quarter of 2024 primarily due to higher shipments, favorable sales price and mix, including

higher metal prices, and favorable foreign exchange translation.

For the first half of 2025, Segment Adjusted EBITDA of $135 million increased 18% compared to the first half of 2024 primarily due to higher shipments and improved Muscle Shoals performance, favorable price and mix

and lower operating costs, partially offset by unfavorable metal costs. Shipments of 545 thousand metric tons increased 4% compared to the first half of 2024 due to higher shipments of packaging rolled products, partially offset by lower

shipments of automotive and specialty rolled products. Revenue of $2.4 billion increased 15% compared to the first half of 2024 primarily due to higher shipments and favorable sales price and mix, including higher metal prices.

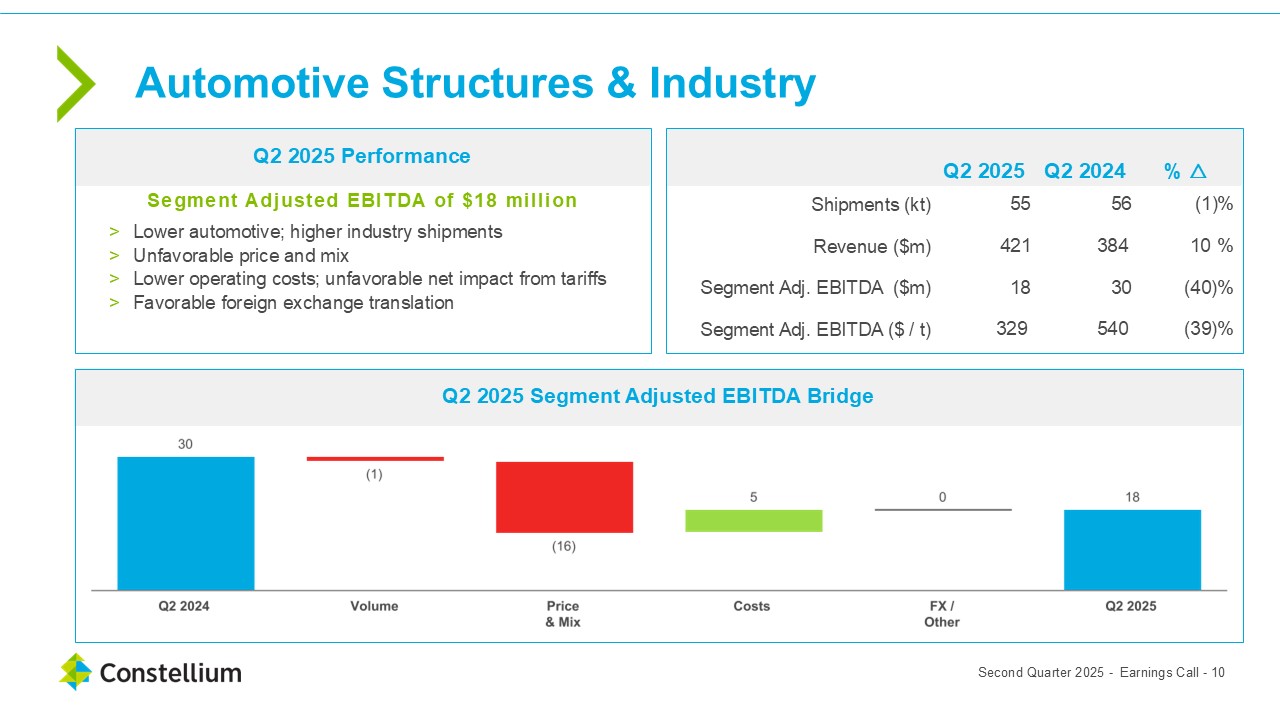

Automotive Structures & Industry (AS&I)

|

Q2 2025

|

Q2 2024

|

Var.

|

YTD

2025

|

YTD

2024

|

Var.

|

|||||||||||||||||||

|

Shipments (k metric tons)

|

55

|

56

|

(1)

|

%

|

107

|

115

|

(7)

|

%

|

||||||||||||||||

|

Revenue ($ millions)

|

421

|

384

|

10

|

%

|

802

|

779

|

3

|

%

|

||||||||||||||||

|

Segment Adjusted EBITDA ($ millions)

|

18

|

30

|

(40)

|

%

|

34

|

63

|

(46)

|

%

|

||||||||||||||||

|

Segment Adjusted EBITDA per metric ton ($)

|

329

|

540

|

(39)

|

%

|

317

|

549

|

(42)

|

%

|

||||||||||||||||

For the second quarter of 2025, Segment Adjusted EBITDA of $18 million decreased 40% compared to the second quarter of 2024 primarily due to unfavorable price and mix and the unfavorable net impact from tariffs,

partially offset by lower operating costs and favorable foreign exchange translation. Shipments of 55 thousand metric tons decreased 1% compared to the second quarter of the prior year due to lower shipments of automotive extruded products mostly

offset by higher shipments of other extruded products. Revenue of $421 million increased 10% compared to the second quarter of 2024 primarily due to favorable sales price and mix, including higher metal prices, and favorable foreign exchange

translation.

For the first half of 2025, Segment Adjusted EBITDA of $34 million decreased 46% compared to the first half of 2024 primarily due to lower shipments, unfavorable price and mix and the unfavorable net impact from

tariffs, partially offset by lower operating costs. Shipments of 107 thousand metric tons decreased 7% compared to the first half of 2024 due to lower shipments of automotive extruded products, partially offset by higher shipments of other

extruded products. Revenue of $802 million increased 3% compared to the first half of 2024 primarily due to favorable sales price and mix, including higher metal prices, partially offset by lower shipments and unfavorable price and mix.

|

5 |

The following table reconciles the total of our segments’ measures of profitability to the group’s net income:

|

Three months ended June 30,

|

Six months ended June 30,

|

|||||||||||||||

|

(in millions of U.S. dollar)

|

2025

|

2024

|

2025

|

2024

|

||||||||||||

|

A&T

|

78

|

90

|

153

|

177

|

||||||||||||

|

P&ARP

|

74

|

66

|

135

|

114

|

||||||||||||

|

AS&I

|

18

|

30

|

34

|

63

|

||||||||||||

|

Holdings and Corporate

|

(12

|

)

|

(6

|

)

|

(23

|

)

|

(14

|

)

|

||||||||

|

Segment Adjusted EBITDA

|

159

|

180

|

299

|

340

|

||||||||||||

|

Metal price lag

|

(13

|

)

|

45

|

33

|

31

|

|||||||||||

|

Adjusted EBITDA

|

146

|

225

|

332

|

371

|

||||||||||||

|

Other adjustments

|

(61

|

)

|

(96

|

)

|

(158

|

)

|

(185

|

)

|

||||||||

|

Finance costs - net

|

(29

|

)

|

(25

|

)

|

(56

|

)

|

(52

|

)

|

||||||||

|

Income before tax

|

56

|

104

|

118

|

134

|

||||||||||||

|

Income tax expense

|

(20

|

)

|

(27

|

)

|

(44

|

)

|

(35

|

)

|

||||||||

|

Net income

|

36

|

77

|

74

|

99

|

||||||||||||

Reconciled items excluded from our Segment Adjusted EBITDA include the following:

Metal price lag

Metal price lag represents the financial impact of the timing difference between when aluminum prices included within Constellium's Revenue are established and when aluminum purchase prices included in Cost of

sales are established, which is a non-cash financial impact. The metal price lag will generally increase our earnings in times of rising primary aluminum prices and decrease our earnings in times of declining primary aluminum prices. The

calculation of metal price lag adjustment is based on a standardized methodology applied at each of Constellium’s manufacturing sites. Metal price lag is calculated as the average value of product purchased in the period, approximated at the

market price, less the value of product in inventory at the weighted average of metal purchased over time, multiplied by the quantity sold in the period.

For the second quarter of 2025, metal price lag was negative, which reflects negative metal price lag in Europe as regional premiums were decreasing, partially offset by positive metal price lag in North America as

regional premiums were increasing. For the first half of 2025, metal price lag was positive, which reflects positive metal price lag in North America as regional premiums were increasing, partially offset by negative metal price lag in Europe as

regional premiums were decreasing. For the second quarter and first half of 2024, metal price lag was positive, which reflects regional premiums increasing during the periods in both North America and Europe.

|

6 |

Other adjustments are detailed in the Reconciliation of net income to Adjusted EBITDA Table on page 19

Net Income

For the second quarter of 2025, net income of $36 million compares to net income of $77 million in the second quarter of the prior year. The decrease in net income is primarily related to lower gross profit

(revenue less cost of sales, excluding depreciation and amortization), higher selling and administrative expenses and unfavorable changes in other gains and losses.

For the first half of 2025, net income of $74 million compares to net income of $99 million in the first half of 2024. The decrease in net income is primarily related to higher depreciation and amortization, and

higher selling and administrative expenses and income tax expense.

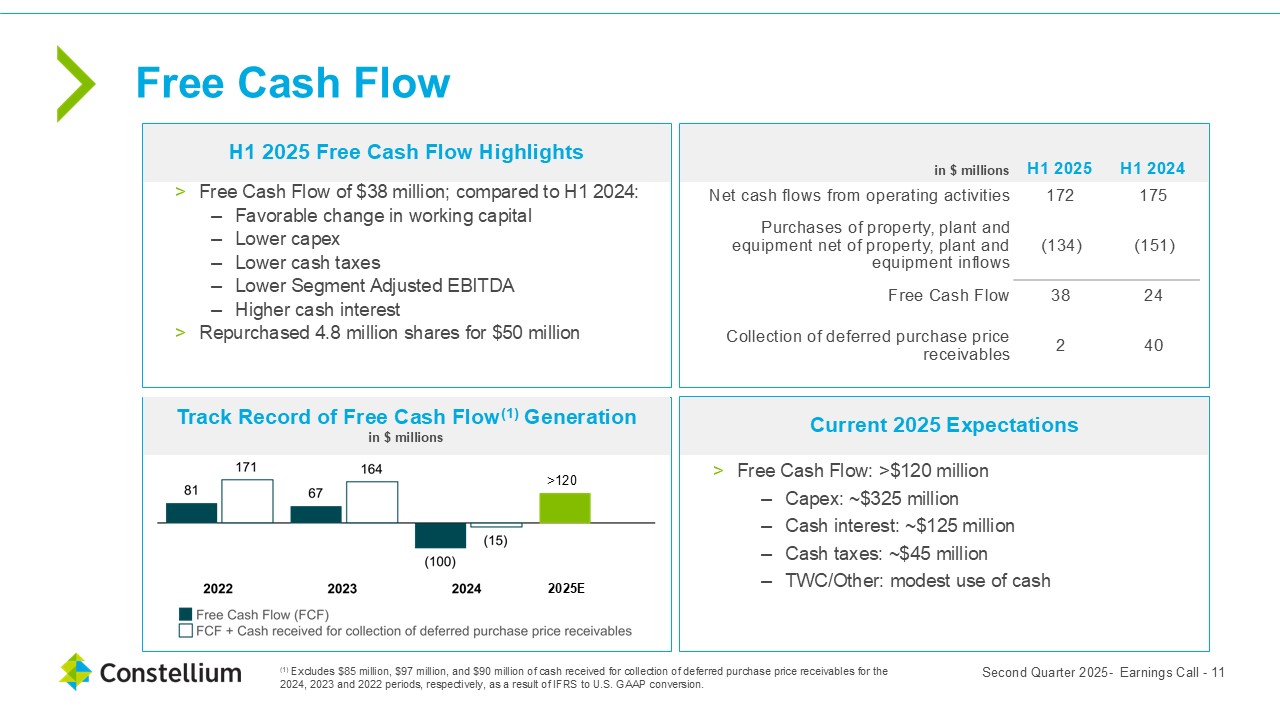

Cash Flow

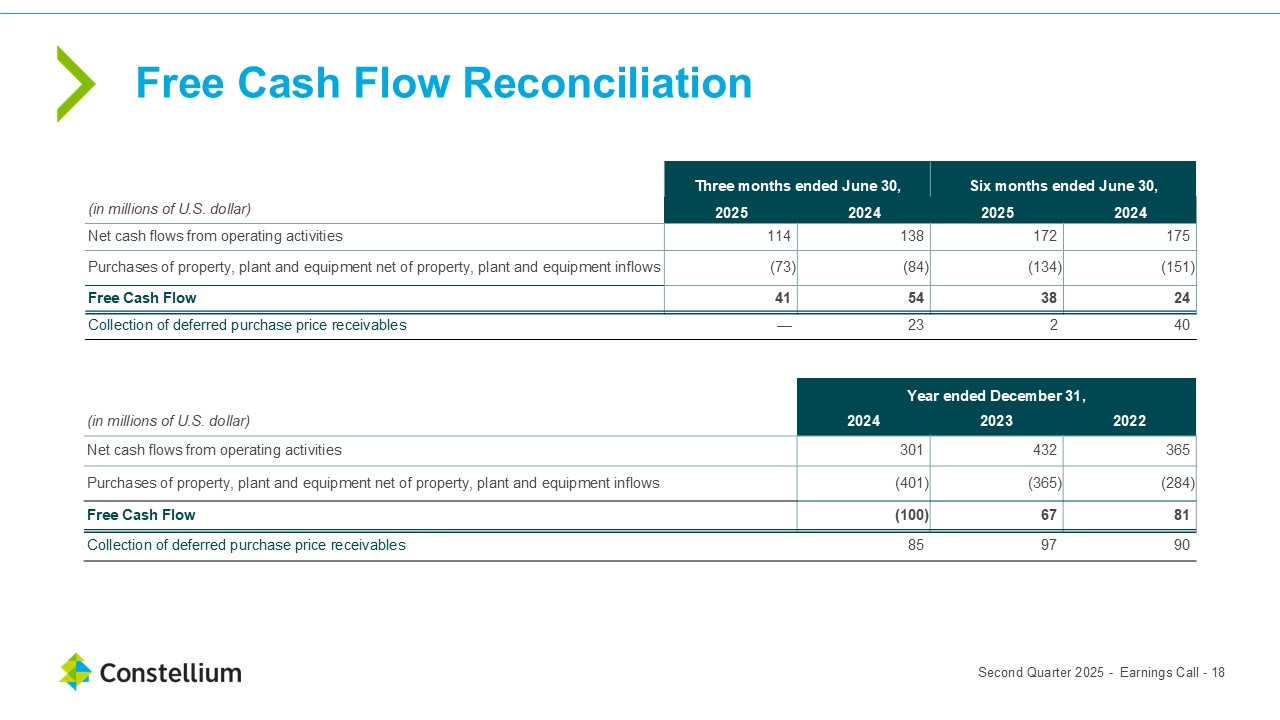

Free Cash Flow was $38 million in the first half of 2025 compared to $24 million in the first half of 2024. The increase in Free Cash Flow was primarily due to a favorable change in working capital, lower capital

expenditures and lower cash taxes, partially offset by lower Segment Adjusted EBITDA and higher cash interest.

Cash flows from operating activities were $172 million for the first half of 2025 compared to cash flows from operating activities of $175 million in the first half of the prior year.

Cash flows used in investing activities were $131 million for the first half of 2025 compared to cash flows used in investing activities of $111 million in the first half of the prior year, which included the

collection of deferred purchase price receivables of $40 million.

Cash flows used in financing activities were $62 million for first half of 2025 compared to cash flows used in financing activities of $51 million in the first half of the prior year. During the first half of 2025,

the Company repurchased 4.8 million shares of the Company stock for $50 million. During the first half of 2024, the Company repurchased 1.9 million shares of the Company stock for $39 million.

|

7 |

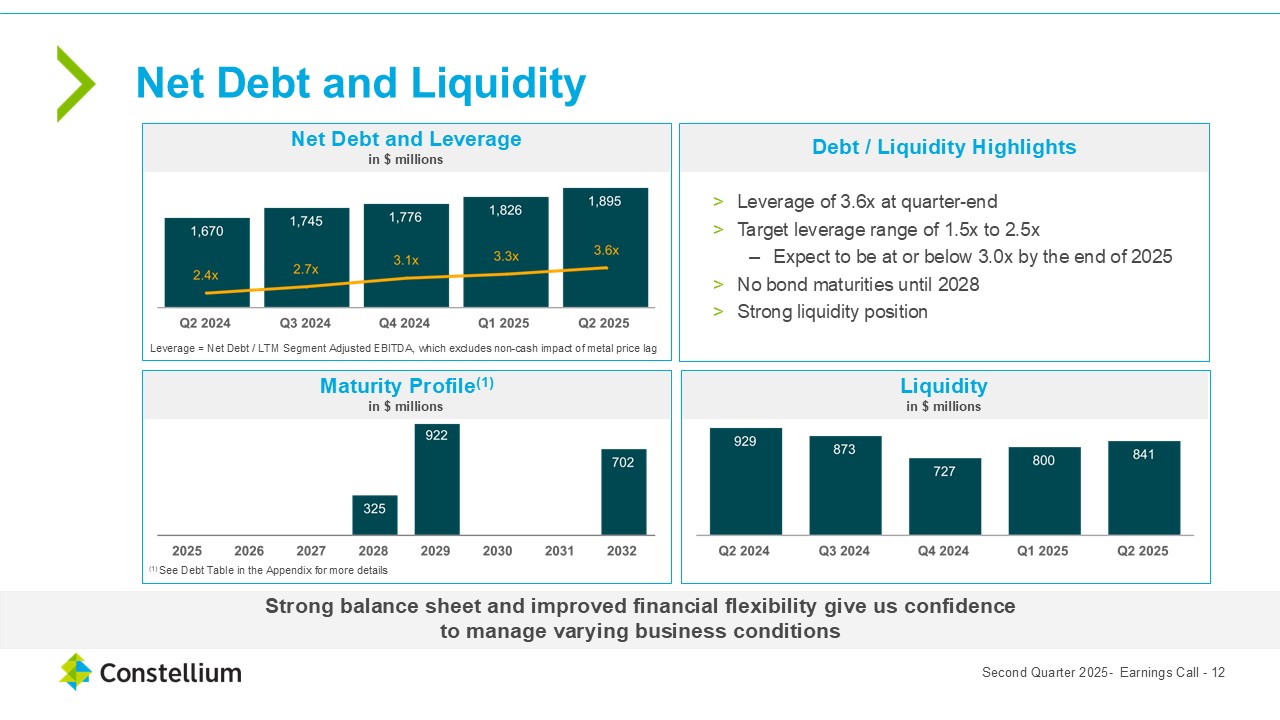

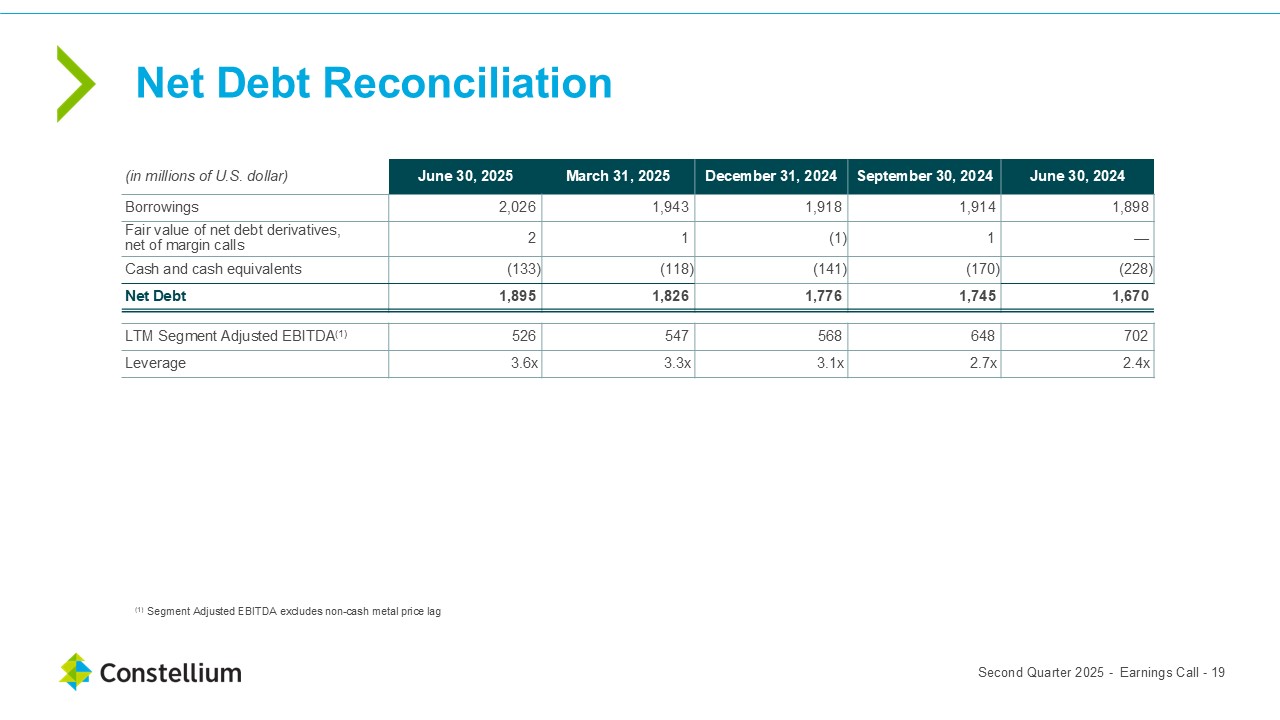

Liquidity and Net Debt

Liquidity at June 30, 2025 was $841 million, comprised of $133 million of cash and cash equivalents and $708 million available under our committed lending facilities and factoring arrangements.

Net debt was $1,895 million at June 30, 2025 compared to $1,776 million at December 31, 2024.

Outlook

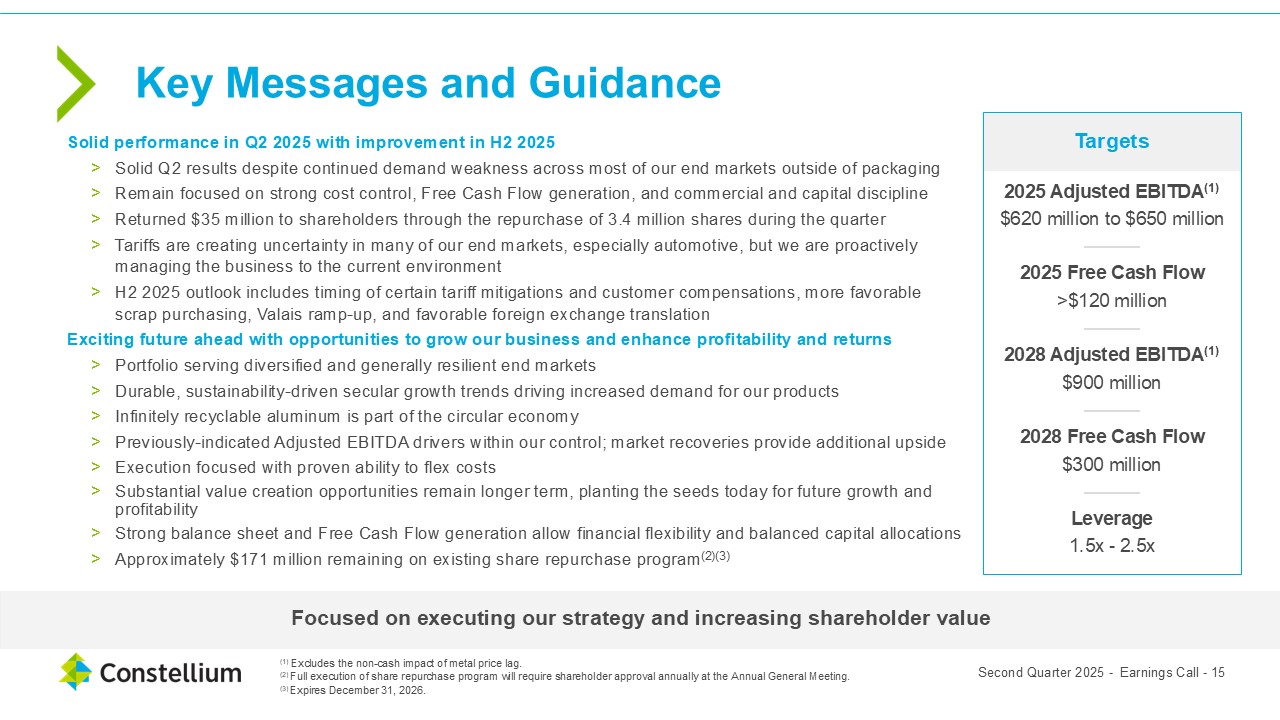

Based on our current outlook, for 2025 we expect Adjusted EBITDA, which excludes the non-cash impact of metal price lag, to be in the range of $620 million to $650 million and Free Cash Flow in excess of $120

million. For 2028, we expect Adjusted EBITDA, which excludes the non-cash impact of metal price lag, of $900 million and Free Cash Flow of $300 million.

We are not able to provide a reconciliation of this Adjusted EBITDA guidance to net income, the comparable GAAP measure, because certain items that are excluded from Adjusted EBITDA cannot be

reasonably predicted or are not in our control. In particular, we are unable to forecast the timing or magnitude of realized and unrealized gains and losses on derivative instruments, impairment or restructuring charges, or taxes without

unreasonable efforts, and these items could significantly impact, either individually or in the aggregate, net income in the future.

Recent Developments

As of June 30, 2025, Constellium no longer qualifies as a Foreign Private Issuer, as determined by Rule 3b-4 under the Securities Exchange Act of 1934. Beginning in 2025, Constellium was already voluntarily

electing to file annual reports on Form 10-K and quarterly reports on Form 10-Q with the Securities and Exchange Commission (“SEC”). Beginning on January 1, 2026, Constellium will continue to file annual reports on Form 10-K and quarterly reports

on Form 10-Q and will also file all other required U.S. domestic forms with the SEC.

|

8 |

Forward-looking statements

Certain statements contained in this press release may constitute forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. This press release may contain

“forward-looking statements” with respect to our business, results of operations and financial condition, and our expectations or beliefs concerning future events and conditions. You can identify forward-looking statements because they contain

words such as, but not limited to, “believes,” “expects,” “may,” “should,” “approximately,” “anticipates,” “estimates,” “intends,” “plans,” “targets,” likely,” “will,” “would,” “could” and similar expressions (or the negative of these

terminologies or expressions). All forward-looking statements involve risks and uncertainties. Many risks and uncertainties are inherent in our industry and markets, while others are more specific to our business and operations. These risks and

uncertainties include, but are not limited to: market competition; economic downturn or industry specific conditions including the impacts of tax and tariff programs, inflation, foreign currency exchange, and industry consolidation; disruption to

business operations; natural disasters including severe flooding and other weather-related events; the conflict between Russia and Ukraine and other geopolitical tensions; the inability to meet customer demand and quality requirements; the loss

of key customers, suppliers or other business relationships; supply disruptions; excessive inflation; the capacity and effectiveness of our hedging policy activities; the loss of key employees; levels of indebtedness which could limit our

operating flexibility and opportunities; and other risk factors set forth under the heading “Risk Factors” in our Annual Report on Form 10-K, and as described from time to time in subsequent reports filed with the U.S. Securities and Exchange

Commission. The occurrence of the events described and the achievement of the expected results depend on many events, some or all of which are not predictable or within our control. Consequently, actual results may differ materially from the

forward-looking statements contained in this press release. We undertake no obligation to update or revise any forward-looking statement as a result of new information, future events or otherwise, except as required by law.

About Constellium

Constellium (NYSE: CSTM) is a global sector leader that develops innovative, value-added aluminum products for a broad scope of markets and applications, including aerospace, packaging and automotive. Constellium

generated $7.3 billion of revenue in 2024.

Constellium’s earnings materials for the second quarter and the first half ended June 30, 2025 are also available on the company’s website (www.constellium.com).

|

9 |

In addition to the results reported in accordance with United States Generally Accepted Accounting Principles (“U.S. GAAP”), this press release includes information regarding certain financial

measures which are not prepared in accordance with U.S. GAAP (“non-GAAP measures”). The non-GAAP measures used in this press release are: Adjusted EBITDA, Free Cash Flow and Net debt. Reconciliations to the most directly comparable U.S. GAAP

financial measures are presented in the schedules to this press release. We believe these non-GAAP measures are important supplemental measures of our operating and financial performance. By providing these measures, together with the

reconciliations, we believe we are enhancing investors’ understanding of our business, our results of operations and our financial position, as well as assisting investors in evaluating the extent to which we are executing our strategic

initiatives. However, these non-GAAP financial measures supplement our U.S. GAAP disclosures and should not be considered an alternative to the U.S. GAAP measures and may not be comparable to similarly titled measures of other companies.

Adjusted EBITDA is not a presentation made in accordance with U.S. GAAP, is not a measure of financial condition, liquidity or profitability and should not be considered as an alternative to profit or loss for the

period, revenues or operating cash flows determined in accordance with U.S. GAAP. The most directly comparable U.S. GAAP measure to Adjusted EBITDA is our net income or loss for the relevant period.

Adjusted EBITDA is defined as income / (loss) from continuing operations before income taxes, results from joint ventures, net finance costs, other expenses and depreciation and amortization as adjusted to exclude

restructuring costs, impairment charges, unrealized gains or losses on derivatives and on foreign exchange differences on transactions which do not qualify for hedge accounting, share based compensation expense, non-operating gains / (losses) on

pension and other post-employment benefits, factoring expenses, effects of certain purchase accounting adjustments, start-up and development costs or acquisition, integration and separation costs, certain incremental costs and other exceptional,

unusual or generally non-recurring items.

We believe Adjusted EBITDA is useful to investors as it illustrates the underlying performance of continuing operations by excluding certain non-recurring and non-operating items. Similar concepts of Adjusted

EBITDA are frequently used by securities analysts, investors and other stakeholders in their evaluation of our company and in comparison, to other companies, many of which present an Adjusted EBITDA-related performance measure when reporting

their results.

|

10 |

Free Cash Flow is defined as net cash flow from operating activities, less capital expenditures, net of property, plant and equipment inflows. Management believes that Free Cash Flow is a useful measure of the net

cash flow generated or used by the business as it takes into account both the cash generated or consumed by operating activities, including working capital, and the capital expenditure requirements of the business. However, Free Cash Flow is not

a presentation made in accordance with U.S. GAAP and should not be considered as an alternative to operating cash flows determined in accordance with U.S. GAAP. Free Cash Flow has certain inherent limitations, including the fact that it does not

represent residual cash flows available for discretionary spending, notably because it does not reflect principal repayments required in connection with our debt or capital lease obligations.

Net debt is defined as debt plus or minus the fair value of cross currency basis swaps net of margin calls less cash and cash equivalents and cash pledged for the issuance of guarantees. Management believes that

Net debt is a useful measure of indebtedness because it takes into account the cash and cash equivalent balances held by the Company as well as the total external debt of the Company. Net debt is not a presentation made in accordance with U.S.

GAAP and should not be considered as an alternative to debt determined in accordance with U.S. GAAP. Leverage is defined as Net debt divided by last twelve months Segment Adjusted EBITDA, which excludes the non-cash impact of metal price lag.

|

11 |

|

Three months ended June 30,

|

Six months ended June 30,

|

|||||||||||||||

|

(in millions of U.S. dollar)

|

2025

|

2024

|

2025

|

2024

|

||||||||||||

|

Revenue

|

2,103

|

1,932

|

4,082

|

3,812

|

||||||||||||

|

Cost of sales (excluding depreciation

and amortization)

|

(1,840

|

)

|

(1,652

|

)

|

(3,556

|

)

|

(3,287

|

)

|

||||||||

|

Depreciation and amortization

|

(82

|

)

|

(76

|

)

|

(160

|

)

|

(151

|

)

|

||||||||

|

Selling and administrative expenses

|

(88

|

)

|

(75

|

)

|

(166

|

)

|

(155

|

)

|

||||||||

|

Research and development expenses

|

(12

|

)

|

(13

|

)

|

(25

|

)

|

(28

|

)

|

||||||||

|

Other gains and losses - net

|

4

|

13

|

(1

|

)

|

(5

|

)

|

||||||||||

|

Finance costs - net

|

(29

|

)

|

(25

|

)

|

(56

|

)

|

(52

|

)

|

||||||||

|

Income before tax

|

56

|

104

|

118

|

134

|

||||||||||||

|

Income tax expense

|

(20

|

)

|

(27

|

)

|

(44

|

)

|

(35

|

)

|

||||||||

|

Net income

|

36

|

77

|

74

|

99

|

||||||||||||

|

Attributable to:

|

||||||||||||||||

|

Equity holders of Constellium

|

36

|

76

|

73

|

97

|

||||||||||||

|

Non-controlling interests

|

—

|

1

|

1

|

2

|

||||||||||||

|

Net income

|

36

|

77

|

74

|

99

|

||||||||||||

|

Earnings per share attributable to the

equity holders of Constellium (in dollars)

|

||||||||||||||||

|

Basic

|

0.25

|

0.52

|

0.51

|

0.66

|

||||||||||||

|

Diluted

|

0.25

|

0.51

|

0.51

|

0.65

|

||||||||||||

|

Weighted average number of shares,

(in thousands)

|

||||||||||||||||

|

Basic

|

140,821

|

146,272

|

141,665

|

146,534

|

||||||||||||

|

Diluted

|

142,244

|

149,233

|

143,174

|

149,722

|

||||||||||||

|

12 |

|

Three months ended June 30,

|

Six months ended June 30,

|

|||||||||||||||

|

(in millions of U.S. dollar)

|

2025

|

2024

|

2025

|

2024

|

||||||||||||

|

Net income

|

36

|

77

|

74

|

99

|

||||||||||||

|

Other comprehensive income / (loss)

|

||||||||||||||||

|

Net change in post-employment benefit obligations

|

—

|

(4

|

)

|

(3

|

)

|

(9

|

)

|

|||||||||

|

Income tax on net change in post-employment benefit obligations

|

(1

|

)

|

—

|

—

|

2

|

|||||||||||

|

Net change in cash flow hedges

|

25

|

(2

|

)

|

37

|

(4

|

)

|

||||||||||

|

Income tax on cash flow hedges

|

(7

|

)

|

1

|

(10

|

)

|

1

|

||||||||||

|

Currency translation adjustments

|

11

|

—

|

15

|

(6

|

)

|

|||||||||||

|

Other comprehensive income / (loss)

|

28

|

(5

|

)

|

39

|

(16

|

)

|

||||||||||

|

Total comprehensive income

|

64

|

72

|

113

|

83

|

||||||||||||

|

Attributable to:

|

||||||||||||||||

|

Equity holders of Constellium

|

63

|

71

|

111

|

81

|

||||||||||||

|

Non-controlling interests

|

1

|

1

|

2

|

2

|

||||||||||||

|

Total comprehensive income

|

64

|

72

|

113

|

83

|

||||||||||||

|

13 |

|

(in millions of U.S. dollar, except share data)

|

At June 30, 2025

|

At December 31, 2024

|

||||||

|

Assets

|

||||||||

|

Current assets

|

||||||||

|

Cash and cash equivalents

|

133

|

141

|

||||||

|

Trade receivables and other, net

|

805

|

486

|

||||||

|

Inventories

|

1,328

|

1,181

|

||||||

|

Fair value of derivatives instruments and other financial assets

|

46

|

26

|

||||||

|

Total current assets

|

2,312

|

1,834

|

||||||

|

Non-current assets

|

||||||||

|

Property, plant and equipment, net

|

2,564

|

2,408

|

||||||

|

Goodwill

|

47

|

46

|

||||||

|

Intangible assets, net

|

93

|

97

|

||||||

|

Deferred tax assets

|

291

|

311

|

||||||

|

Trade receivables and other, net

|

40

|

36

|

||||||

|

Fair value of derivatives instruments

|

21

|

2

|

||||||

|

Total non-current assets

|

3,056

|

2,900

|

||||||

|

Total assets

|

5,368

|

4,734

|

||||||

|

Liabilities

|

||||||||

|

Current liabilities

|

||||||||

|

Trade payables and other

|

1,717

|

1,309

|

||||||

|

Current portion of long-term debt

|

54

|

39

|

||||||

|

Fair value of derivatives instruments

|

32

|

33

|

||||||

|

Income tax payable

|

18

|

18

|

||||||

|

Pension and other benefit obligations

|

24

|

22

|

||||||

|

Provisions

|

28

|

25

|

||||||

|

Total current liabilities

|

1,873

|

1,446

|

||||||

|

Non-current liabilities

|

||||||||

|

Trade payables and other

|

169

|

156

|

||||||

|

Long-term debt

|

1,972

|

1,879

|

||||||

|

Fair value of derivatives instruments

|

3

|

21

|

||||||

|

Pension and other benefit obligations

|

394

|

375

|

||||||

|

Provisions

|

94

|

91

|

||||||

|

Deferred tax liabilities

|

64

|

39

|

||||||

|

Total non-current liabilities

|

2,696

|

2,561

|

||||||

|

Total liabilities

|

4,569

|

4,007

|

||||||

|

Commitments and contingencies

|

||||||||

|

Shareholder's equity

|

||||||||

|

Ordinary shares, par value €0.02, 146,819,884 shares issued at June 30, 2025 and 2024

|

4

|

4

|

||||||

|

Additional paid in capital

|

513

|

513

|

||||||

|

Accumulated other comprehensive income

|

26

|

(14

|

)

|

|||||

|

Retained earnings and other reserves

|

237

|

203

|

||||||

|

Equity attributable to equity holders of Constellium

|

780

|

706

|

||||||

|

Non-controlling interests

|

19

|

21

|

||||||

|

Total equity

|

799

|

727

|

||||||

|

Total equity and liabilities

|

5,368

|

4,734

|

||||||

|

14 |

CONSOLIDATED STATEMENTS OF CHANGES IN EQUITY (unaudited)

|

(in millions of U.S. dollar)

|

Ordinary

shares

|

Additional

paid in

capital

|

Treasury

shares

|

Accumulated

other

comprehensive

income / (loss)

|

Other

reserves

|

Retained

earnings

|

Total

|

Non-

controlling

interests

|

Total

equity

|

|||||||||||||||||||||||||||

|

At January 1, 2025

|

4

|

513

|

(51

|

)

|

(14

|

)

|

161

|

93

|

706

|

21

|

727

|

|||||||||||||||||||||||||

|

Net income

|

—

|

—

|

—

|

—

|

—

|

37

|

37

|

1

|

38

|

|||||||||||||||||||||||||||

|

Other comprehensive income

|

—

|

—

|

—

|

11

|

—

|

—

|

11

|

—

|

11

|

|||||||||||||||||||||||||||

|

Total comprehensive income

|

—

|

—

|

—

|

11

|

—

|

37

|

48

|

1

|

49

|

|||||||||||||||||||||||||||

|

Share-based compensation

|

—

|

—

|

—

|

—

|

6

|

—

|

6

|

—

|

6

|

|||||||||||||||||||||||||||

|

Repurchase of ordinary shares

|

—

|

—

|

(15

|

)

|

—

|

—

|

—

|

(15

|

)

|

—

|

(15

|

)

|

||||||||||||||||||||||||

|

Allocation of treasury shares to share-based compensation plan vested

|

—

|

—

|

12

|

—

|

—

|

(12

|

)

|

—

|

—

|

—

|

||||||||||||||||||||||||||

|

Other

|

—

|

—

|

—

|

2

|

—

|

(2

|

)

|

—

|

—

|

—

|

||||||||||||||||||||||||||

|

Transactions with non-controlling interests

|

—

|

—

|

—

|

—

|

—

|

—

|

—

|

(2

|

)

|

(2

|

)

|

|||||||||||||||||||||||||

|

At March 31, 2025

|

4

|

513

|

(54

|

)

|

(1

|

)

|

167

|

116

|

745

|

20

|

765

|

|||||||||||||||||||||||||

|

Net income

|

—

|

—

|

—

|

—

|

—

|

36

|

36

|

—

|

36

|

|||||||||||||||||||||||||||

|

Other comprehensive income

|

—

|

—

|

—

|

27

|

—

|

—

|

27

|

1

|

28

|

|||||||||||||||||||||||||||

|

Total comprehensive income

|

—

|

—

|

—

|

27

|

—

|

36

|

63

|

1

|

64

|

|||||||||||||||||||||||||||

|

Share-based compensation

|

—

|

—

|

—

|

—

|

7

|

—

|

7

|

—

|

7

|

|||||||||||||||||||||||||||

|

Repurchase of ordinary shares

|

—

|

—

|

(35

|

)

|

—

|

—

|

—

|

(35

|

)

|

—

|

(35

|

)

|

||||||||||||||||||||||||

|

Allocation of treasury shares to share-based compensation plan vested

|

—

|

—

|

—

|

—

|

—

|

—

|

—

|

—

|

—

|

|||||||||||||||||||||||||||

|

Other

|

—

|

—

|

—

|

—

|

—

|

—

|

—

|

—

|

—

|

|||||||||||||||||||||||||||

|

Transactions with non-controlling interests

|

—

|

—

|

—

|

—

|

—

|

—

|

—

|

(2

|

)

|

(2

|

)

|

|||||||||||||||||||||||||

|

At June 30, 2025

|

4

|

513

|

(89

|

)

|

26

|

174

|

152

|

780

|

19

|

799

|

||||||||||||||||||||||||||

|

15 |

|

(in millions of U.S. dollar)

|

Ordinary

shares

|

Additional

paid in

capital

|

Treasury

shares

|

Accumulated

other

comprehensive

income / (loss)

|

Other

reserves

|

Retained

earnings

|

Total

|

Non-

controlling

interests

|

Total

equity |

|||||||||||||||||||||||||||

|

At January 1, 2024

|

4

|

513

|

—

|

—

|

136

|

65

|

718

|

24

|

742

|

|||||||||||||||||||||||||||

|

Net income

|

—

|

—

|

—

|

—

|

—

|

21

|

21

|

1

|

22

|

|||||||||||||||||||||||||||

|

Other comprehensive loss

|

—

|

—

|

—

|

(11

|

)

|

—

|

—

|

(11

|

)

|

—

|

(11

|

)

|

||||||||||||||||||||||||

|

Total comprehensive (loss) / income

|

—

|

—

|

—

|

(11

|

)

|

—

|

21

|

10

|

1

|

11

|

||||||||||||||||||||||||||

|

Share-based compensation

|

—

|

—

|

—

|

—

|

6

|

—

|

6

|

—

|

6

|

|||||||||||||||||||||||||||

|

Repurchase of ordinary shares

|

—

|

—

|

(7

|

)

|

—

|

—

|

—

|

(7

|

)

|

—

|

(7

|

)

|

||||||||||||||||||||||||

|

Allocation of treasury shares to share-based compensation plan vested

|

—

|

—

|

—

|

—

|

—

|

—

|

—

|

—

|

—

|

|||||||||||||||||||||||||||

|

Transactions with non-controlling interests

|

—

|

—

|

—

|

—

|

—

|

—

|

—

|

(1

|

)

|

(1

|

)

|

|||||||||||||||||||||||||

|

At March 31, 2024

|

4

|

513

|

(7

|

)

|

(11

|

)

|

142

|

86

|

727

|

24

|

751

|

|||||||||||||||||||||||||

|

Net income

|

—

|

—

|

—

|

—

|

—

|

76

|

76

|

1

|

77

|

|||||||||||||||||||||||||||

|

Other comprehensive loss

|

—

|

—

|

—

|

(5

|

)

|

—

|

—

|

(5

|

)

|

—

|

(5

|

)

|

||||||||||||||||||||||||

|

Total comprehensive (loss) / income

|

—

|

—

|

—

|

(5

|

)

|

—

|

76

|

71

|

1

|

72

|

||||||||||||||||||||||||||

|

Share-based compensation

|

—

|

—

|

—

|

—

|

7

|

—

|

7

|

—

|

7

|

|||||||||||||||||||||||||||

|

Repurchase of ordinary shares

|

—

|

—

|

(32

|

)

|

—

|

—

|

—

|

(32

|

)

|

—

|

(32

|

)

|

||||||||||||||||||||||||

|

Allocation of treasury shares to share-based compensation plan vested

|

—

|

—

|

28

|

—

|

—

|

(28

|

)

|

—

|

—

|

—

|

||||||||||||||||||||||||||

|

Transactions with non-controlling interests

|

—

|

—

|

—

|

—

|

—

|

—

|

—

|

(2

|

)

|

(2

|

)

|

|||||||||||||||||||||||||

|

At June 30, 2024

|

4

|

513

|

(11

|

)

|

(16

|

)

|

149

|

134

|

773

|

23

|

796

|

|||||||||||||||||||||||||

|

16 |

|

Three months ended June 30,

|

Six months ended June 30,

|

|||||||||||||||

|

(in millions of U.S. dollar)

|

2025

|

2024

|

2025

|

2024

|

||||||||||||

|

Net income

|

36

|

77

|

74

|

99

|

||||||||||||

|

Adjustments

|

||||||||||||||||

|

Depreciation and amortization

|

82

|

76

|

160

|

151

|

||||||||||||

|

Impairment of assets

|

—

|

5

|

—

|

8

|

||||||||||||

|

Pension and other long-term benefits

|

2

|

2

|

4

|

4

|

||||||||||||

|

Finance costs - net

|

29

|

25

|

56

|

52

|

||||||||||||

|

Income tax expense

|

20

|

27

|

44

|

35

|

||||||||||||

|

Unrealized gains on derivatives - net and from remeasurement of monetary assets and liabilities - net

|

(35

|

)

|

(4

|

)

|

(24

|

)

|

(1

|

)

|

||||||||

|

Losses on disposal

|

1

|

—

|

1

|

1

|

||||||||||||

|

Other - net

|

11

|

13

|

22

|

26

|

||||||||||||

|

Changes in working capital

|

||||||||||||||||

|

Inventories

|

4

|

(43

|

)

|

(65

|

)

|

(27

|

)

|

|||||||||

|

Trade receivables

|

12

|

(68

|

)

|

(261

|

)

|

(241

|

)

|

|||||||||

|

Trade payables

|

(38

|

)

|

64

|

241

|

164

|

|||||||||||

|

Other

|

23

|

12

|

5

|

(4

|

)

|

|||||||||||

|

Change in provisions

|

(1

|

)

|

—

|

(2

|

)

|

(2

|

)

|

|||||||||

|

Pension and other long-term benefits paid

|

(12

|

)

|

(12

|

)

|

(25

|

)

|

(22

|

)

|

||||||||

|

Interest paid

|

(24

|

)

|

(20

|

)

|

(53

|

)

|

(46

|

)

|

||||||||

|

Income tax paid

|

4

|

(16

|

)

|

(5

|

)

|

(22

|

)

|

|||||||||

|

Net cash flows from operating activities

|

114

|

138

|

172

|

175

|

||||||||||||

|

Purchases of property, plant and equipment

|

(77

|

)

|

(84

|

)

|

(146

|

)

|

(158

|

)

|

||||||||

|

Property, plant and equipment inflows

|

4

|

—

|

12

|

7

|

||||||||||||

|

Collection of deferred purchase price receivable

|

—

|

23

|

2

|

40

|

||||||||||||

|

Other investing activities

|

1

|

—

|

1

|

—

|

||||||||||||

|

Net cash flows used in investing activities

|

(72

|

)

|

(61

|

)

|

(131

|

)

|

(111

|

)

|

||||||||

|

Repurchase of ordinary shares

|

(35

|

)

|

(32

|

)

|

(50

|

)

|

(39

|

)

|

||||||||

|

Repayments of long-term debt

|

(2

|

)

|

(3

|

)

|

(3

|

)

|

(5

|

)

|

||||||||

|

Net change in revolving credit facilities and short-term debt

|

23

|

(1

|

)

|

28

|

—

|

|||||||||||

|

Finance lease repayments

|

(1

|

)

|

(3

|

)

|

(3

|

)

|

(5

|

)

|

||||||||

|

Transactions with non-controlling interests

|

(2

|

)

|

(2

|

)

|

(4

|

)

|

(3

|

)

|

||||||||

|

Other financing activities

|

(19

|

)

|

—

|

(30

|

)

|

1

|

||||||||||

|

Net cash flows used in financing activities

|

(36

|

)

|

(41

|

)

|

(62

|

)

|

(51

|

)

|

||||||||

|

Net increase / (decrease) in cash and cash equivalents

|

6

|

36

|

(21

|

)

|

13

|

|||||||||||

|

Cash and cash equivalents - beginning of the period

|

118

|

194

|

141

|

223

|

||||||||||||

|

Net increase / (decrease) in cash and cash equivalents

|

6

|

36

|

(21

|

)

|

13

|

|||||||||||

|

Effect of exchange rate changes on cash and cash equivalents

|

9

|

(2

|

)

|

13

|

(8

|

)

|

||||||||||

|

Cash and cash equivalents - end of period

|

133

|

228

|

133

|

228

|

||||||||||||

|

17 |

SEGMENT ADJUSTED EBITDA

|

Three months ended June 30,

|

Six months ended June 30,

|

|||||||||||||||

|

(in millions of U.S. dollar)

|

2025

|

2024

|

2025

|

2024

|

||||||||||||

|

A&T

|

78

|

90

|

153

|

177

|

||||||||||||

|

P&ARP

|

74

|

66

|

135

|

114

|

||||||||||||

|

AS&I

|

18

|

30

|

34

|

63

|

||||||||||||

|

Holdings and Corporate

|

(12

|

)

|

(6

|

)

|

(23

|

)

|

(14

|

)

|

||||||||

|

Three months ended June 30,

|

Six months ended June 30,

|

|||||||||||||||

|

(in k metric tons)

|

2025

|

2024

|

2025

|

2024

|

||||||||||||

|

Aerospace rolled products

|

22

|

25

|

46

|

52

|

||||||||||||

|

Transportation, industry, defense and other rolled products

|

31

|

35

|

59

|

65

|

||||||||||||

|

Packaging rolled products

|

213

|

187

|

417

|

374

|

||||||||||||

|

Automotive rolled products

|

59

|

69

|

119

|

140

|

||||||||||||

|

Specialty and other thin-rolled products

|

6

|

6

|

10

|

12

|

||||||||||||

|

Automotive extruded products

|

29

|

33

|

60

|

69

|

||||||||||||

|

Other extruded products

|

25

|

22

|

47

|

45

|

||||||||||||

|

Total shipments

|

384

|

378

|

756

|

758

|

||||||||||||

|

Three months ended June 30,

|

Six months ended June 30,

|

|||||||||||||||

|

(in millions of U.S. dollar)

|

2025

|

2024

|

2025

|

2024

|

||||||||||||

|

Aerospace rolled products

|

267

|

262

|

534

|

548

|

||||||||||||

|

Transportation, industry, defense and other rolled products

|

226

|

225

|

427

|

418

|

||||||||||||

|

Packaging rolled products

|

912

|

729

|

1,780

|

1,400

|

||||||||||||

|

Automotive rolled products

|

295

|

319

|

586

|

631

|

||||||||||||

|

Specialty and other thin-rolled products

|

27

|

30

|

55

|

66

|

||||||||||||

|

Automotive extruded products

|

249

|

251

|

483

|

514

|

||||||||||||

|

Other extruded products

|

173

|

133

|

320

|

266

|

||||||||||||

|

Other and inter-segment eliminations

|

(45

|

)

|

(17

|

)

|

(102

|

)

|

(30

|

)

|

||||||||

|

Total Revenue by product line

|

2,103

|

1,932

|

4,082

|

3,812

|

||||||||||||

Amounts may not sum due to rounding.

|

18 |

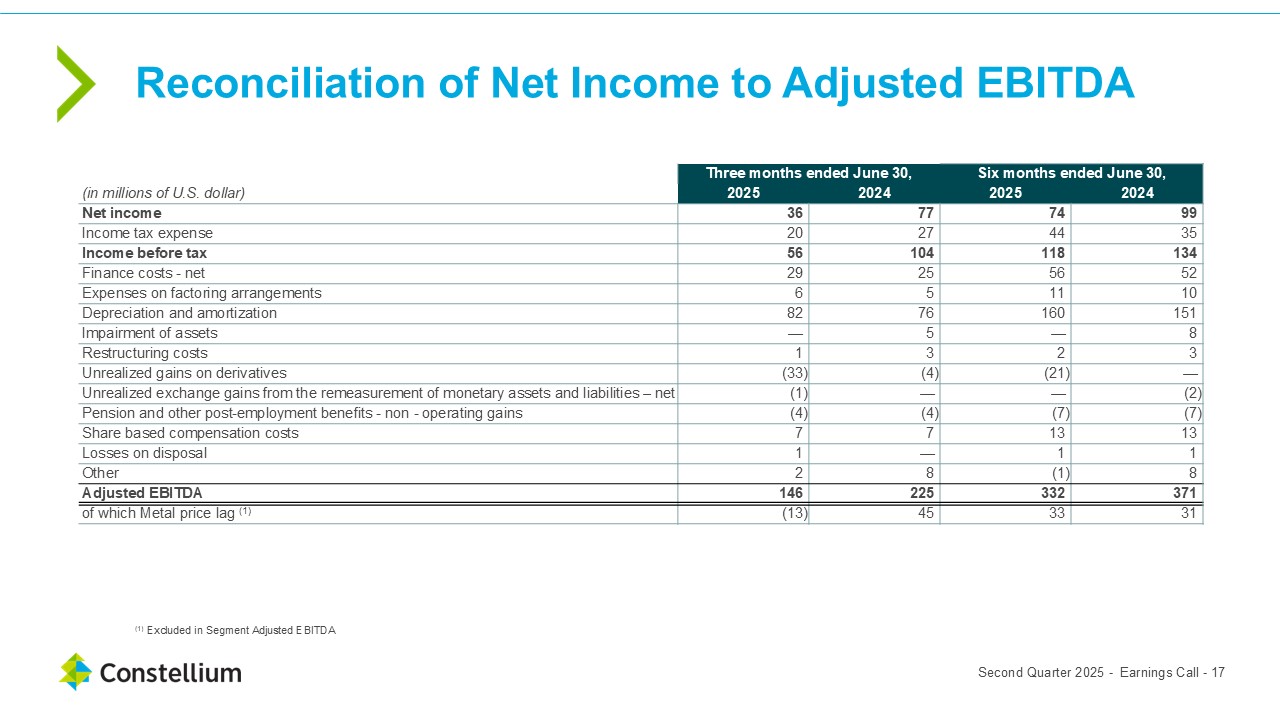

Reconciliation of net income to Adjusted EBITDA (a non-GAAP measure)

|

Three months ended June 30,

|

Six months ended June 30,

|

|||||||||||||||

|

(in millions of U.S. dollar)

|

2025

|

2024

|

2025

|

2024

|

||||||||||||

|

Net income

|

36

|

77

|

74

|

99

|

||||||||||||

|

Income tax expense

|

20

|

27

|

44

|

35

|

||||||||||||

|

Finance costs - net

|

29

|

25

|

56

|

52

|

||||||||||||

|

Expenses on factoring arrangements

|

6

|

5

|

11

|

10

|

||||||||||||

|

Depreciation and amortization

|

82

|

76

|

160

|

151

|

||||||||||||

|

Impairment of assets (B)

|

—

|

5

|

—

|

8

|

||||||||||||

|

Restructuring costs

|

1

|

3

|

2

|

3

|

||||||||||||

|

Unrealized gains on derivatives

|

(33

|

)

|

(4

|

)

|

(21

|

)

|

—

|

|||||||||

|

Unrealized exchange gains from the remeasurement of monetary assets and liabilities – net

|

(1

|

)

|

—

|

—

|

(2

|

)

|

||||||||||

|

Pension and other post-employment benefits - non - operating gains

|

(4

|

)

|

(4

|

)

|

(7

|

)

|

(7

|

)

|

||||||||

|

Share based compensation costs

|

7

|

7

|

13

|

13

|

||||||||||||

|

Losses / (gains) on disposal

|

1

|

—

|

1

|

1

|

||||||||||||

|

Other (C)

|

2

|

8

|

(1

|

)

|

8

|

|||||||||||

|

Adjusted EBITDA1

|

146

|

225

|

332

|

371

|

||||||||||||

|

of which Metal price lag (A)

|

(13

|

)

|

45

|

33

|

31

|

|||||||||||

1Adjusted EBITDA includes the non-cash impact of metal price lag

| (A) |

Metal price lag represents the financial impact of the timing difference between when aluminum prices included within Constellium's Revenue are established and when aluminum purchase prices included in Cost of sales are established,

which is a non-cash financial impact. The metal price lag will generally increase our earnings in times of rising primary aluminum prices and decrease our earnings in times of declining primary aluminum prices. The calculation of metal

price lag adjustment is based on a standardized methodology applied at each of Constellium’s manufacturing sites. Metal price lag is calculated as the average value of product purchased in the period, approximated at the market price,

less the value of product in inventory at the weighted average of metal purchased over time, multiplied by the quantity sold in the period.

|

| (B) |

For the three and six months ended June 30, 2024, impairment related to property, plant and equipment in our Valais operations.

|

| (C) |

For the three months ended June 30, 2025, other mainly includes $2 million of clean-up costs related to the flooding of our facilities in Valais (Switzerland). For the six months ended June 30, 2025, Other mainly includes $9 million of

insurance proceeds and $7 million of clean-up costs related to the flooding of our facilities in Valais (Switzerland). For the three and six months ended June 30, 2024, other was related to $6 million of inventory impairment as a result

of the flooding of our facilities in Valais (Switzerland) at the end of June 2024 as well as $2 million of costs associated with non-recurring corporate transformation projects.

|

|

19 |

|

Three months ended June 30,

|

Six months ended June 30,

|

|||||||||||||||

|

(in millions of U.S. dollar)

|

2025

|

2024

|

2025

|

2024

|

||||||||||||

|

Net cash flows from operating activities

|

114

|

138

|

172

|

175

|

||||||||||||

|

Purchases of property, plant and equipment

|

(77

|

)

|

(84

|

)

|

(146

|

)

|

(158

|

)

|

||||||||

|

Property, plant and equipment inflows

|

4

|

—

|

12

|

7

|

||||||||||||

|

Free Cash Flow

|

41

|

54

|

38

|

24

|

||||||||||||

Reconciliation of borrowings to Net debt (a non-GAAP measure)

|

(in millions of U.S. dollar)

|

At June 30, 2025

|

At December 31, 2024

|

||||||

|

Debt

|

2,026

|

1,918

|

||||||

|

Fair value of cross currency basis swaps,

net of margin calls

|

2

|

(1

|

)

|

|||||

|

Cash and cash equivalents

|

(133

|

)

|

(141

|

)

|

||||

|

Net debt

|

1,895

|

1,776

|

||||||

|

20 |